Accounts receivable and payable accounting is not just about tracking receivables and payables; it's also a vital cash flow management tool for commercial enterprises. In the context of 2025, with the roadmap for implementing new accounting regulations and interest rate pressures, scientific accounts receivable management helps businesses limit bad debts, improve liquidity, and enhance their reputation with partners. This article provides a comprehensive guide to accounts receivable and payable accounting, from concepts and accounts to accounting procedures and the latest digital transformation trends.

What is accounts payable accounting?

Debt accounting (often divided into Accounts Receivable and Accounts Payable) is a branch of accounting that tracks and controls accounts receivable from customers and accounts payable to suppliers and partners.

The role of accounts payable in a business.

Managing and controlling accounts receivable plays a crucial role in maintaining stable cash flow, directly impacting business performance and the company's reputation with customers and partners. In this context, accounts receivable accountants perform the following important roles:

- Monitoring, analyzing, and evaluating the financial status related to accounts receivable and payable, thereby providing a database to advise and support leadership in making appropriate management decisions.

- Compiling and providing detailed information on accounts receivable and payable helps the management team build and adjust financial strategies effectively.

- Record all payment transactions accurately and promptly for each party, and monitor payment progress to ensure obligations are fulfilled on time and to prevent misappropriation of funds.

- Regularly check and reconcile accounts receivable, especially for customers with high transaction frequency or large balances, to ensure transparency and mitigate financial risks.

- Participating in controlling and minimizing bad debts contributes to improving capital efficiency and maintaining financial stability and security for businesses.

Although debt plays a crucial role in controlling cash flow and stabilizing finances, it continues to arise throughout a business's operations. So, what are the core reasons behind this situation?

Causes of accounts receivable/payable in business operations

Accounts payable in businesses arise from various causes, linked to financial activities and business policies, including:

- The company has not yet allocated sufficient funds to pay for goods and services purchased from suppliers within the agreed timeframe.

- Customers incur debt because they lack the financial capacity to immediately pay for the goods and services they have used.

- To expand market share and increase sales, the company adopted a sales policy that allows customers to receive goods first and pay later.

Some types of goods or services are agreed to be paid for after the delivery or acceptance process is complete. - The buyer prioritizes using borrowed capital with lower interest rates, leading to extended payment terms for the partner.

From the causes of accounts receivable mentioned above, it can be seen that accounts receivable does not only appear with a specific group of entities but is directly related to many subjects in business operations. Therefore, clearly identifying the entities that need to be monitored for accounts receivable is a crucial step in helping businesses control financial obligations, limit risks, and ensure the accuracy of accounting data.

The entity responsible for monitoring accounts receivable/payable.

In a corporate accounting system, liabilities are reflected through the following main accounts:

- Accounts receivable from customers (Account 131): Records amounts of money that the business has provided goods and services for but has not yet received from customers.

- Accounts Payable to Suppliers (Account 331): Reflects the company's payment obligations to suppliers of goods and services.

- Internal advances and reimbursements (Account 141): Tracks funds that the enterprise temporarily provides to employees to support production and business activities, and the subsequent reimbursement.

- Other receivables (Account 138): Includes liabilities arising outside of normal sales relationships, such as compensation, deposits, collateral, or recovery of missing assets.

- Other payables and liabilities (Account 338): Records other financial obligations of the enterprise such as insurance, union fees, or amounts received for safekeeping or deposits.

- Intercompany receivables (Account 136): Tracks accounts payable arising between the parent company and its branches, subsidiaries, or between units within the same system.

- Internal payables (Account 336): Reflects internal payment obligations between the company and its subsidiaries within the same enterprise.

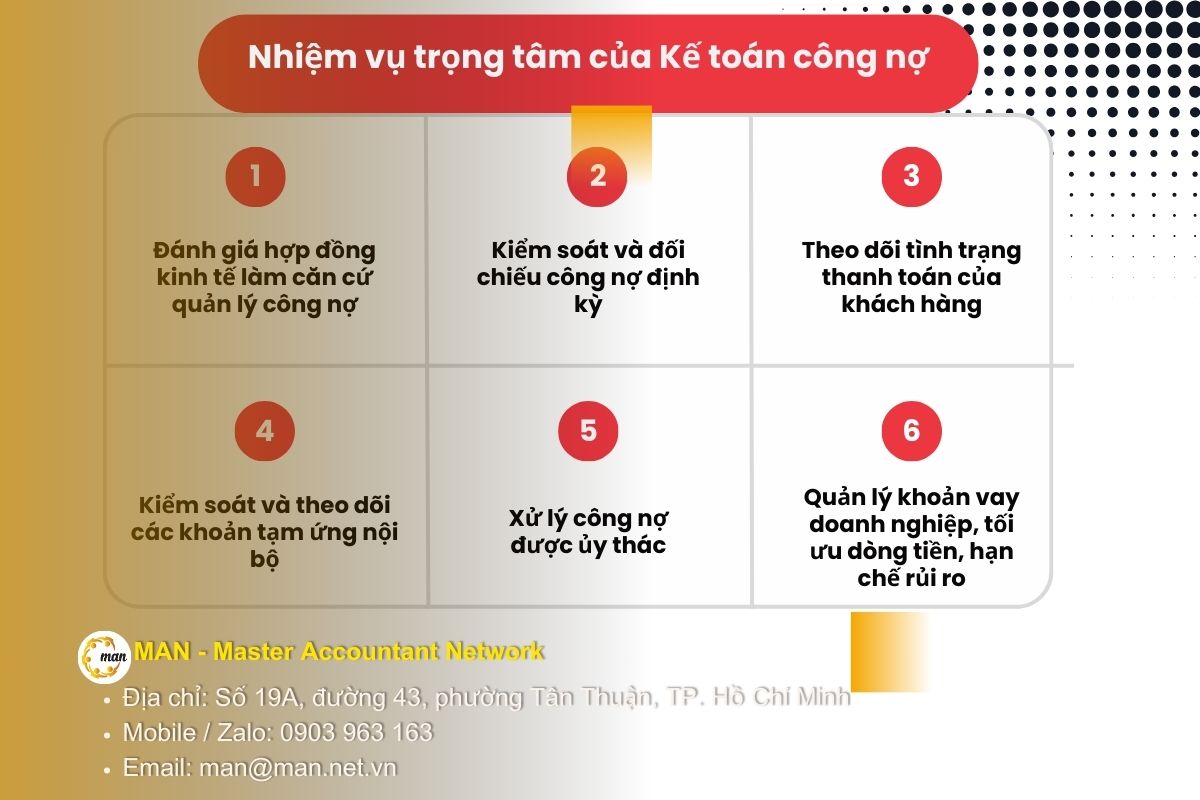

The core responsibilities of Accounts Payable Accountant

The main responsibilities of an Accounts Payable Accountant primarily involve managing accounts payable and bad debts, specifically:

Evaluating economic contracts as a basis for managing accounts receivable.

During the implementation process, the accountant will be responsible for the following:

- Ensure that all information regarding suppliers, customers, and new partners is fully recorded and updated in the accounting software or relevant management system.

- Timely adjustment and updating of customer and supplier data when changes occur, such as transfers, legal changes, or transaction information.

- Carefully review the payment terms in contracts with each partner, customer, and supplier to minimize the risk of errors and ensure compliance with signed agreements.

Regularly monitor and reconcile accounts receivable.

To effectively control accounts receivable and minimize risks, accountants need to perform the following tasks:

- Review all order information thoroughly, including the granted credit limit and payment terms, based on the sales contract signed with the customer and partner.

- Carefully compare the details related to the type of goods, actual quantity delivered, selling price, and payment terms for contracts that are currently being executed or have already been completed.

- Track and manage the detailed accounts receivable and payable status of each customer, partner, and supplier, focusing on due dates, amounts paid, and any overdue debts.

- Compile and evaluate the results of accounts receivable audits and report them promptly to relevant departments or management for appropriate action.

Track customer payment status.

When accounts receivable arise from economic contracts or sales invoices, accounts receivable accountants are responsible for updating and monitoring the payment progress of each customer and related partner.

Control and monitor internal advances.

To ensure financial discipline and stable cash flow within the business, the following key tasks are being implemented:

- Closely monitor the payment progress of each individual and department within the company, updating and reminding them of outstanding debts on a daily basis.

- Regularly review advances that are due or overdue, compile a summary list, and proactively follow up on payments weekly or as directed by management.

Debt collection is handled through a delegated agency.

Specifically, the accounting operations performed include:

- Record financial transactions based on valid invoices, ensuring that their nature and timing are accurately reflected in the accounting records.

- Based on the economic contract and related documents, review and adjust any discrepancies or inaccuracies in unit prices, quantities, or payment values.

- Manage and track detailed accounts receivable and payable for each customer, partner, or related party to control potential risks.

- Review, compile, and print accounting documents for internal reconciliation with the accounting manager or control department.

Managing business loans aims to optimize cash flow and mitigate risks.

The key tasks to be performed include:

- Complete the liquidation of finished contracts, and update and manage new contracts as related financial transactions arise.

- Closely monitor payment progress, proactively remind and urge parties to fulfill their payment obligations on time as committed in the contract.

- Record transactions and adjust necessary journal entries to ensure accounting figures reflect the actual exchange rate at the time of recording.

- In cases where a business incurs interest payments, the accountant needs to accurately determine the amount, prepare all necessary documentation, and forward it to the relevant departments for payment according to each contract and specific party.

Building upon the overall framework of accounts receivable management, the following section will focus on clarifying the accounting procedures for accounts receivable and how to effectively monitor them.

Accounts Receivable Accountant

What are accounts receivable?

Accounts receivable are amounts of money that a business is entitled to collect from customers or related parties, arising from the provision of goods, services, or advances made by the business but not yet received at the time of recognition.

The liabilities incurred include:

- Accounts receivable are debts incurred when customers purchase products or services but have not yet made payment.

- Internal receivables: These are amounts that a business must collect when financial or commercial relationships arise with subordinate entities or branches of the business.

- Other receivables include: advances, deposits, collateral, and amounts receivable from individuals or groups that have already been settled as compensation, etc.

Based on the nature of accounts receivable, accountants need to apply appropriate procedures for tracking, accounting for, and managing accounts receivable.

Accounts Receivable Accounting Procedures

In a business, the role of an accounts receivable accountant is to ensure that payments are collected correctly, in full, and on time.

Related documents

The following are important documents and records that are required:

- Economic contract/Purchase order.

- Electronic invoice (e-Invoice).

- Delivery note/Warehouse release form.

- Payment documents (Credit advice, receipt).

Basic accounting procedures

When selling goods but not yet receiving payment:

- Debit Account 131

- There is account 511 (Revenue).

- There is account 3331 (VAT payable)

When collecting debts:

- Debit accounts 111 and 112

- There is account 131.

Processing payment discounts for customers:

- Debit Account 635 (Financial Expenses)

- There is account 131.

Accounts Payable Accountant

What are accounts payable?

Liabilities are amounts of money that a business is obligated to pay to suppliers, partners, and employees, arising from economic transactions but not yet paid at the time of accounting.

Based on payment terms, accounts payable to suppliers are categorized into two main groups:

- Short-term liabilities: These are financial obligations that a business must pay within no more than 12 months from the date of recognition. This group includes items such as interest payable, salaries and wages owed to employees, advances or deposits from customers, as well as accounts payable arising from sales relationships with suppliers.

- Long-term liabilities: These are debts and financial obligations with a repayment period of more than 12 months, such as loans for production and business operations, mortgage loans, or short-term debts with agreed-upon payment extensions.

In addition to debts to external partners, businesses also incur internal liabilities during their operations, including:

- Receivables, payables, payments, or disbursements between independent accounting units within the same system, arising when one unit makes payments or collects payments on behalf of another unit within the enterprise.

- Financial obligations to the State and related parties include: amounts payable to the state budget, loans, deposits received, internal debts, social insurance and health insurance contributions for employees, and union fees as stipulated.

To effectively manage accounts payable, accountants need to have a thorough understanding of accounting procedures and the tracking of accounts payable for each relevant party.

Accounts Payable Accounting Procedures

This involves controlling a company's financial obligations to third parties. Effective management of accounts payable helps businesses optimize the use of capital from suppliers.

Accounts Payable Accounting Process

When purchasing goods for inventory:

- Debit accounts 152, 156, 642

- Debit Account 1331 (Input VAT)

- There is account 331.

When paying off debts:

- Debit account 331

- There are accounts 111 and 112.

Receive purchase discounts from our partners:

- Debit account 331

- There is account 515 (Financial revenue) or a deduction from the value of purchased goods.

Provision for doubtful receivables

According to Circular 48/2019/TT-BTCRegarding the provision for doubtful receivables, the amount is determined based on the overdue period of the debt, specifically as follows:

| Overdue | Provisioning level |

| From 6 months to less than 1 year | 30% debt value |

| From 1 year to less than 2 years | 50% debt value |

| From 2 years to less than 3 years | 70% debt value |

| From 3 years or more | 100% debt value |

Note: For telecommunications or retail businesses with a large amount of small-scale debt, a percentage-based estimation method of the total outstanding debt may be applied.

Conclude

Accounts receivable and payable accounting plays a particularly important role in accurately reflecting the financial situation and protecting the cash flow of a business. Closely monitoring accounts receivable and payable, reconciling accounts payable periodically, and making provisions in accordance with regulations not only helps limit the risk of bad debt but also enhances long-term financial management capabilities.

In the context of increasingly stringent accounting regulations and rising liquidity pressures, businesses need to develop a systematic accounts payable accounting process, keep up-to-date with new regulations, and apply technology for more effective management.

If your business needs advice, review, or standardization of accounts payable accounting practices, don't hesitate to contact the expert team at MAN – Master Accountant Network for support tailored to your specific business operations.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about Accounts Payable

What are the differences between accounts payable and accounts payable?

Accounts payable focuses on cash inflows and outflows (cash or bank receipts and disbursements), while accounts payable focuses on obligations to pay and obligations to collect (tracking outstanding balances).

What should be done if the customer refuses to sign the debt reconciliation statement?

If the client does not confirm the transaction, the accountant should retain alternative documents such as: contracts, invoices, delivery receipts, payment documents, and email correspondence. These are still accepted as valid evidence when explaining matters to tax authorities or auditors.

Is it mandatory to reconcile accounts payable and receivable with customers and suppliers?

Reconciliation of accounts payable is not a mandatory procedure, but it is a crucial requirement in accounting and auditing practice. Regular reconciliation helps to detect discrepancies promptly, reduce disputes, and provides evidence for verifying accounts payable balances during tax settlements or financial statement audits.

Is it possible to offset accounts receivable and accounts payable against the same party?

Debt offsetting should only be carried out when both parties have a clear written agreement and sufficient legal basis. In the accounting records, accounts receivable and accounts payable must still be tracked separately before offsetting.

MAN Editorial Board – Master Accountant Network