Preparing financial statements is a crucial step that determines the transparency, credibility, and governance capacity of each business in 2026. This is a time when accounting regulations are becoming increasingly stringent, and the adoption of international standards such as IFRS is being strongly promoted in Vietnam under the direction of the Ministry of Finance. This article provides comprehensive guidance, from determining the applicable accounting system and the 7-step process for preparing professional financial statements to online submission through the electronic tax system, as well as common errors and penalties to avoid. If businesses want to ensure accurate data, comply with the law, and optimize their value in the eyes of banks and investors, this is an indispensable guide.

Regulations to note when preparing financial statements

To prepare financial statements that comply with regulations and ensure transparency, businesses need to clearly understand the core information that must be presented. This information not only reflects the overall financial picture but also serves as a basis for regulators, investors, and banks to assess the stability and effectiveness of the business's operations.

Financial reports must provide information about:

- Assets: All resources that the business is managing and using at the time of reporting.

- Liabilities: Financial obligations that arise and for which a business is responsible for payment.

- Equity: The remaining value belonging to the owner after deducting liabilities.

- Revenue and other income: Items that increase economic benefits during the period.

- Production and business expenses and other expenses: Items that reduce economic benefits during the course of operations.

- Business results (profit or loss) and the distribution of after-tax profits.

- Cash flows: Cash inflows and outflows from operating activities, investing, and financing.

In addition to the main criteria, businesses need to add:

- Clearly explain the nature of the items presented.

- Describe the accounting policies applied when recording economic transactions.

- Clarify any unusual fluctuations between periods.

Requirements regarding the principles of drafting and presentation:

- The report must be prepared within the legally prescribed deadline.

- The data must be clear, transparent, easy to understand, and highly reliable.

- Financial information must be continuously reflected across periods, ensuring comparability.

- The report must be based on closed-end accounting data and adhere strictly to the principles and methods prescribed by current regulations.

- The presentation must be consistent across accounting periods.

- If there are any changes to the methodology or presentation, the business must provide full explanation and clearly state the reasons for the adjustments.

See more: Financial Reporting Services

The importance of preparing financial statements.

Preparing financial statements is the process of compiling data from detailed accounting records and the general ledger to present the financial position, business results, and cash flows of a business during an accounting period.

The year 2026 marks a significant turning point as many businesses begin piloting or becoming required to transition to International Financial Reporting Standards (IFRS). Accurate financial reporting helps businesses:

- Avoid administrative penalties for tax and accounting violations.

- Providing reliable data to banks and investors to raise capital.

- It helps management gain insightful views into the company's "health" so they can adjust strategies in a timely manner.

Applicable legal framework and accounting system

To prepare financial statements in accordance with regulations, accountants need to clearly identify which legal document applies to their business:

- Circular 200/2014/TT-BTC: Applicable to all types of businesses, especially large-scale businesses requiring detailed documentation and accounting systems.

- Circular 133/2016/TT-BTC: Accounting regime for small and medium-sized enterprises (SMEs), focusing on simplicity and efficiency.

- Circular 132/2018/TT-BTC: Specific guidance for micro-enterprises, omitting many complex reports such as the Cash Flow Statement.

Note 2026: Listed corporations and FDI enterprises need to pay attention to the roadmap for adopting VFRS (New Vietnamese Financial Reporting Standards), which is gradually approaching full compliance with IFRS.

What does a complete set of financial statements include?

Depending on the applicable regulations, the set of documents for preparing financial statements will include:

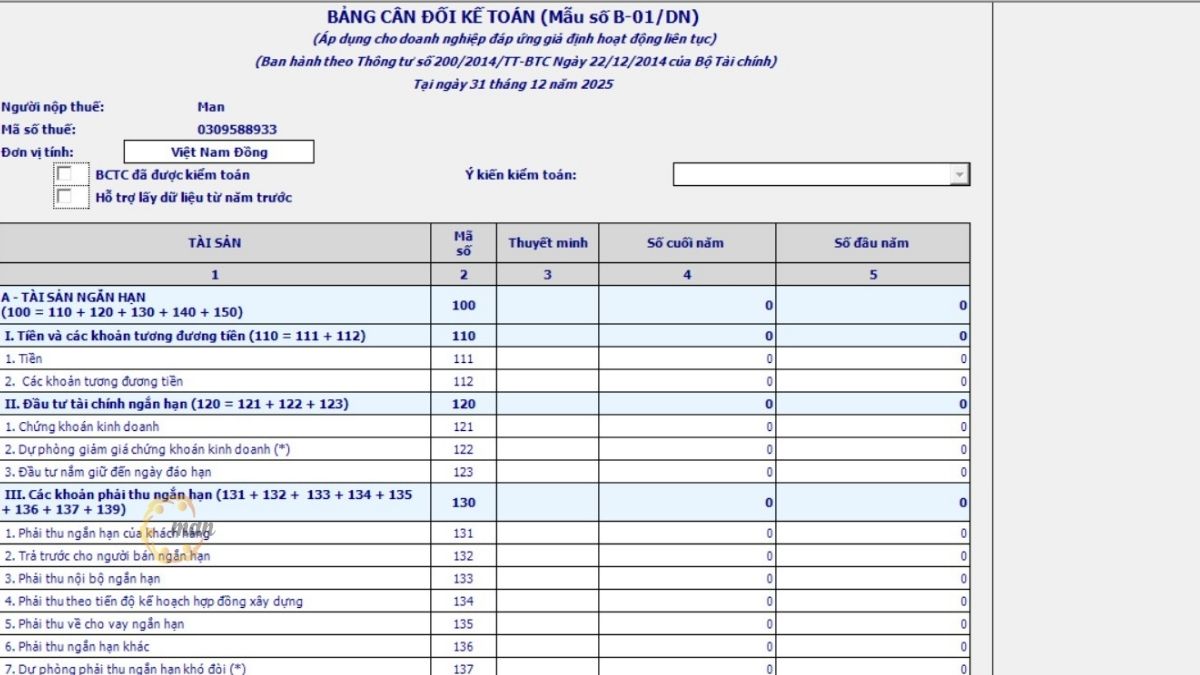

- Financial Statement (Balance Sheet): Provides an overview of the value of assets and liabilities at a specific point in time.

- Income statement: Presents revenue, expenses, and profit for the period.

- Cash flow statement: Explains the fluctuations in cash from operating activities, investing, and financing.

- Notes to the Financial Statements: Provide detailed information on accounting policies and explain significant financial fluctuations.

- Trial Balance: (Required for businesses applying Circular 133/2016/TT-BTC).

A guide on how to prepare professional financial statements.

To ensure accurate and logical financial statement preparation, and to minimize the risk of errors, businesses need to follow a systematic process, from initial document processing to the compilation and completion of the final explanatory notes. Below are specific steps for preparing professional financial statements that accountants need to follow sequentially and closely monitor at each stage.

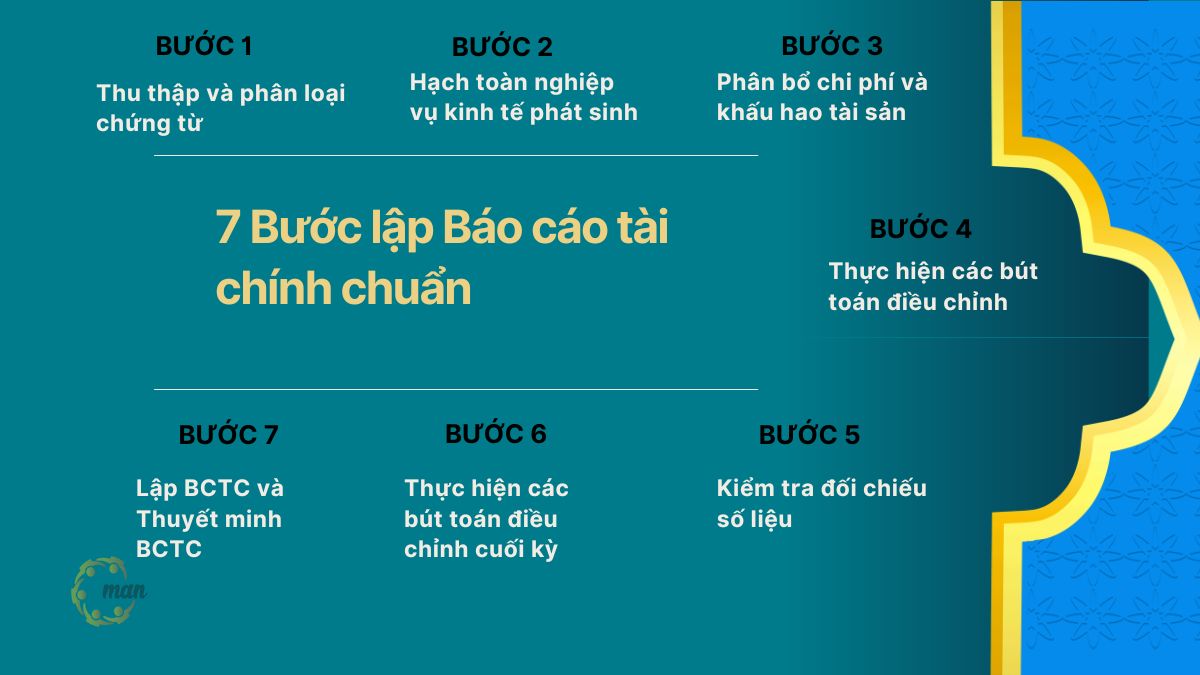

Step 1 – Collect and classify documents

This is the foundation of preparing financial statements. Accountants need to collect all outgoing and incoming invoices, receipts, payment vouchers, debit notes, and credit notes from banks. Ensure the "Reasonable - Valid - Legal" nature of each invoice before entering the data.

Step 2 – Recording economic transactions that occur

After completing the sorting and verification of documents, the accountant begins the process of recording accounting data.

Specifically, economic transactions will be reflected in detailed and summary accounting records in accordance with the applicable accounting system and accounting standards. Accounting must ensure that the transactions accurately reflect their nature, comply with legal regulations, and truthfully and fully represent the actual business operations of the enterprise.

This process can be done using Excel in the case of small businesses, or through specialized accounting software to increase accuracy, reduce errors, and improve data processing efficiency.

Step 3 – Allocate costs and depreciate assets

To ensure proper accounting period recognition and cost allocation, businesses need to follow these steps:

First, prepaid expenses such as installment office rent, insurance premiums, major repair costs, etc., must be gradually allocated over the actual benefit period, avoiding recording the entire amount in a single period which would distort business results.

For fixed assets, businesses need to determine the appropriate depreciation method (straight-line, declining balance, based on production output, etc.) based on the asset's usage characteristics and the regulations in Circular 45/2013/TT-BTC (or any replacement document if applicable). The chosen method must ensure consistency across periods and accurately reflect the economic depreciation of the asset.

When using accounting software, accountants need to enter complete information about the original cost, useful life, and the start date of depreciation or expense allocation into the corresponding modules. Simultaneously, a separate tracking table should be created in Excel to monitor depreciation and prepaid expense allocation. Regularly comparing the software data with the external tracking table will help minimize errors and allow for timely adjustments if discrepancies arise.

For businesses specializing in manufacturing, construction, or project management, a detailed cost allocation spreadsheet in Excel may be necessary for better internal management and to track each component of cost in more detail.

Specifically:

- Direct costs such as salaries, insurance (social security, health insurance), outsourced service costs, etc., need to be clearly allocated to each product code, contract, or project to ensure accuracy in cost calculation.

- Indirect costs such as business management costs, sales costs, etc., should be allocated appropriately to each department, division, or cost center to facilitate performance analysis.

Proper allocation and depreciation not only helps financial statements accurately reflect the financial situation but also supports management in controlling costs and making more accurate operational decisions.

Step 4 – Make adjusting entries

Before closing the books and preparing the financial statements, accountants need to proactively check, review, and make necessary adjusting entries to ensure that the figures accurately and fairly reflect the financial situation. Specifically:

- Re-evaluate exchange rate differences at the end of the period: Determine and record monetary items denominated in foreign currency at the year-end exchange rate, and account for exchange rate gains/losses according to current regulations.

- Provisioning for doubtful debts: Review and fully record items such as doubtful receivables, inventory devaluation, trading securities devaluation, or investment losses, etc. The provisions must be based on clear grounds and supported by complete documentation.

- Recording expenses to be accrued in advance for the fiscal year: For expenses that have been incurred but not yet paid, accrual should be made in advance, such as 13th-month salary, Tet holiday bonus, year-end audit fees, rent, utilities, and raw materials or recurring service fees.

- Adjusting Unearned Revenue: Review temporarily recognized revenue items (e.g., promotional programs, customer appreciation programs, long-term service contracts, etc.) to determine the portion of revenue eligible for recognition in the period and make appropriate transfers.

- Perform reclassification entries: Ensure accurate representation of the nature and timing on the financial statements, including reclassifying investments, adjusting overdrafts, classifying short-term and long-term liabilities, and reclassifying loans according to their remaining terms.

- Correction of errors (if detected): If errors are detected during the accounting process, corrective entries must be made promptly before issuing the financial statements to avoid affecting accuracy and legal compliance.

Completing these review and adjustment steps will ensure that the end-of-period accounting figures accurately reflect the company's true situation, minimizing risks during tax settlements or independent audits.

Step 5 – Verify and compare the data

After completing the recording of all transactions, accountants need to conduct a comprehensive review of the data to ensure accuracy and consistency before preparing the financial statements.

- Compare the detailed ledger and the summary ledger for each account to ensure that the transactions and the ending balance match.

- Review the balances of key accounts such as accounts receivable, accounts payable, cash on hand, bank deposits, inventory, etc., in order to promptly detect discrepancies or under-recordings.

- Cross-referencing with relevant records and reports, including: accounts payable and receivable reports, payroll records, cash book, inventory records, bank reconciliation statements, etc., is necessary to ensure that accounting data accurately reflects reality.

- Address and adjust any discrepancies (if any) immediately before closing the books to avoid affecting the accuracy of the final financial statements.

This verification step acts as a “final control layer,” helping to minimize the risk of errors and ensure that the data is eligible for inclusion in the report.

Step 6 – Perform year-end closing entries

Perform journal entries to transfer the balances of accounts type 5 to type 9 to account 911 (Determining business results).

- Debit Account 511 / Credit Account 911.

- Debit account 911 / Credit accounts 632, 641, 642…

For businesses that incur corporate income tax payable, the accountant needs to make the first transfer to determine the profit, calculate the tax payable, and record additional entries to recognize the tax and tax expense incurred. Then, the transfer is repeated to arrive at the final profit figure.

- Calculate the corporate income tax payable (Debit Account 821 / Credit Account 3334).

Step 7 – Prepare Financial Statements and Notes to the Financial Statements

Once all accounting data has been reviewed and confirmed to accurately and completely reflect all transactions that occurred during the period, the accountant proceeds to the aggregation step to prepare the financial statements. This is the stage of transferring data from the accounting system to the prescribed reporting forms.

According to Circular 200/2014/TT-BTC, this financial reporting regime applies to businesses in all sectors and types of activities, regardless of size. Therefore, strict adherence to the form structure and presentation principles is mandatory.

In cases where businesses use Excel for accounting, accountants need to rely on the Trial Balance to compile data and manually fill in each item in the Statement of Financial Position, Statement of Income, and related forms. This process requires a high degree of care to avoid discrepancies between total assets and total liabilities or between pre-tax and after-tax profits.

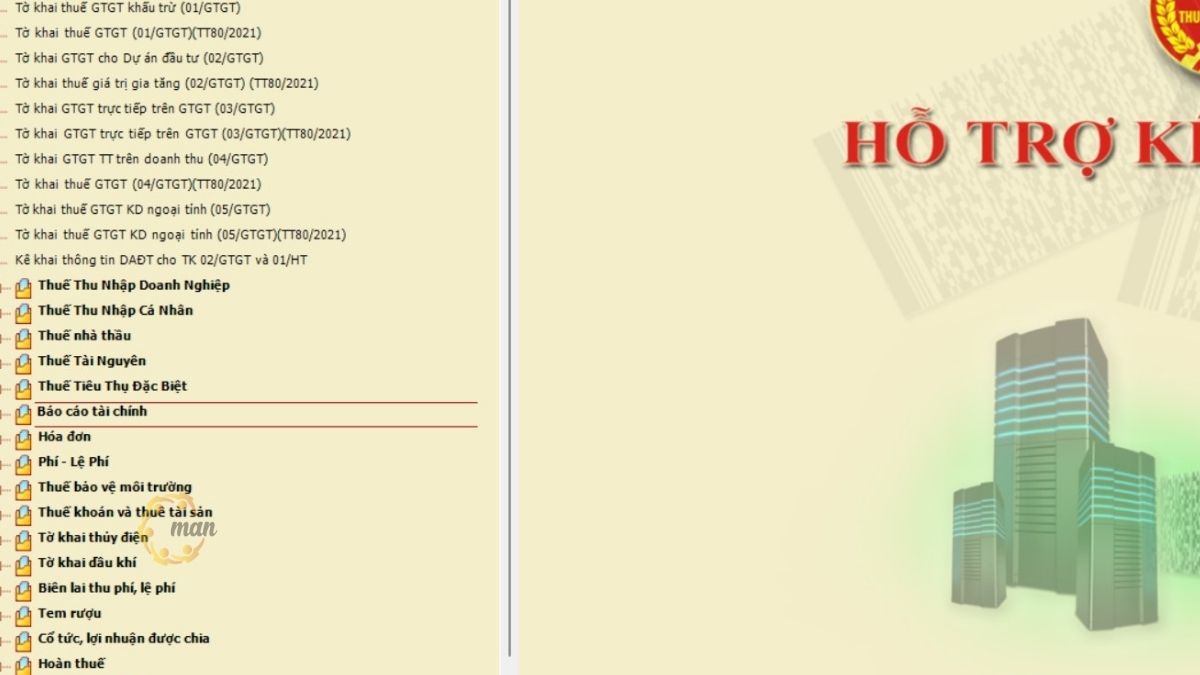

After completing the internal report, the accountant prepares and submits the financial statements using the HTKK software in accordance with the prescribed procedures. The steps will be performed sequentially as follows:

- Log in using your registered business account.

- Select the "Financial Statements" option. This step will vary for each business depending on the accounting policies applied, in order to select the appropriate financial statements.

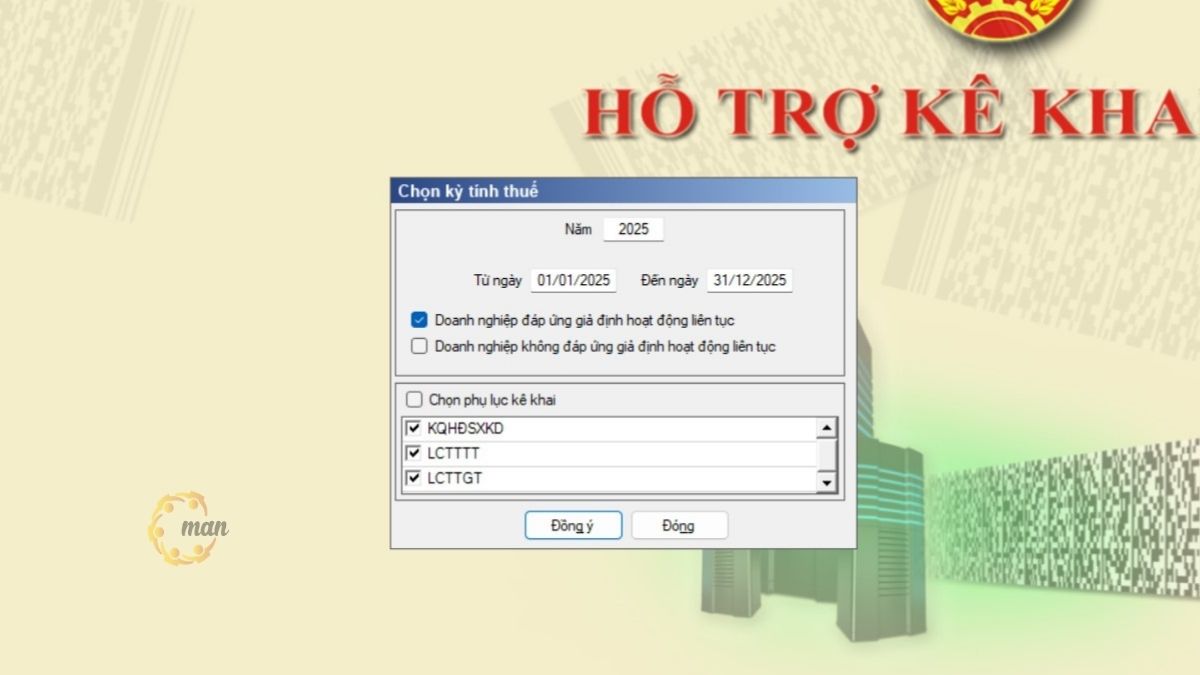

- Next, select the "Financial Year" feature. Here, you need to complete entering all the information and then select "Agree" for the Declaration form interface to appear.

- On the Declaration form interface, businesses need to fill in all the required information in all three forms: Balance Sheet, Income Statement, and Cash Flow Statement. Once you've finished, click the "Save" button and wait for the message "Data saved successfully!" to appear on the screen.

- The final step is simply to "Export XML" and save the completed exported file to your computer to use as accounting data for submission to the tax authorities. That completes the steps for preparing financial statements using the HTKK software.

Deadline for submitting financial statements and penalties for violations.

The deadline for preparing and submitting financial statements to the authorities is usually:

For state-owned enterprises

Regarding the deadline for submitting quarterly financial reports:

- The deadline for submitting quarterly financial reports is within 20 days. from the end of the quarterly accounting period; parent companies and state-owned corporations are granted a maximum extension of 45 days;

- Accounting units under state-owned enterprises and corporations submit quarterly financial reports to the parent company or corporation within the deadlines stipulated by the parent company or corporation..

Regarding the deadline for submitting annual financial statements:

- The deadline for submitting annual financial statements is within 30 days. from the end of the quarterly accounting period; however, parent companies and state-owned corporations are allowed to submit the payment no later than 90 days.

- Accounting units directly under state-owned corporations are required to submit annual financial reports to the parent company or the corporation within the deadlines stipulated by the superior authority.

For other types of businesses

Private enterprises and partnerships must submit their annual financial statements within 30 days of the end of the fiscal year; for other types of businesses, the deadline is no more than 90 days.

Note: According to Decree 125/2020/ND-CP, the penalty for late submission of financial statements can range from VND 5,000,000 to VND 15,000,000. In cases of serious violations or data falsification, the penalty can reach VND 50,000,000 and lead to the seizure of invoices.

Conclude

Preparing financial statements is not just a final closing step at the end of the period, but also a comprehensive process encompassing a company's management capabilities, risk control, and legal compliance. When done correctly according to legal regulations, businesses not only avoid penalties but also build a transparent financial foundation, creating an advantage when working with banks, investors, and strategic partners.

In the context of 2026, with increasingly stringent data standardization requirements and a trend towards international standards, proactively reviewing financial reporting processes, applying software, and updating new policies is essential. If a business lacks a specialized team or wants to optimize time, cost, and accuracy, collaborating with a consulting and supply unit is a viable option. professional accounting services This would be a safe and effective solution.

Standardizing financial statements today is a solid foundation for sustainable growth tomorrow.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about Preparing Financial Statements

To clarify more about financial reporting services, here are the most common questions:

Do businesses that don't generate revenue need to prepare financial statements?

Yes. Even if no revenue or business activity is generated during the period, the enterprise must still prepare and submit financial statements within the deadlines stipulated by the Accounting Law No. 88/2015/QH13.

Is it possible to create financial statements using Excel instead of accounting software?

Permitted. However, when using Excel, accountants must ensure: The figures match the Trial Balance, there are no discrepancies between Total Assets and Total Liabilities, and there is a logical connection between accounting profit and tax. Afterward, the data must still be re-entered into the HTKK software to generate XML and submit it through the electronic tax system.

Can the submitted financial statements be adjusted?

Yes. Businesses are allowed to resubmit replacement financial statements if errors are discovered, provided that the Tax Authority has not yet issued a decision to conduct an inspection or audit at the company's premises.

When should you hire a financial reporting service?

Businesses should consider hiring accounting services when: They lack in-house accounting expertise; they are preparing for loans, audits, or fundraising; they are preparing to transition to IFRS; or there are discrepancies in data from multiple years that need correction. Proactively addressing these issues from the outset will help minimize legal risks and avoid significant corrective costs later on.