Checking and preparing the Trial Balance is the most important "final step" before a business prepares its financial statements and tax returns for 2026. A trial balance not only needs to be balanced numerically (Total Debit = Total Credit) but also must be accurate in terms of the nature of the transactions and comply with the regulations of the Accounting Law No. 88/2015/QH13, Circular 200/2014/TT-BTC, Circular 133/2016/TT-BTC, and Circular 99/2025/TT-BTC.

In the context of digital accounting and AI-powered automated reconciliation, the role of accountants has not diminished but has shifted to risk control, discrepancy analysis, and ensuring data transparency. This article will help you understand the standard process, advanced auditing techniques, and the latest updates to ensure that auditing and preparing the Trial Balance truly becomes an effective financial management tool, rather than just a formality.

What is a trial balance?

The trial balance is a comprehensive accounting report that shows all increases, decreases, and current balances of assets, liabilities, and equity during an accounting period, and reflects the cumulative figures from the beginning of the year to the reporting date. This is a crucial document that helps businesses verify the accuracy of their accounting records, serving as a basis for comparison and control of data before preparing financial statements.

From a detailed perspective, the Trial Balance also shows the fluctuations of each accounting account during the period. This allows accountants to check the completeness and reasonableness of recorded transactions, detect discrepancies if any, and ensure that the data in the books matches the data presented in the financial reporting system.

See more: Financial Reporting Services

Sample trial balance

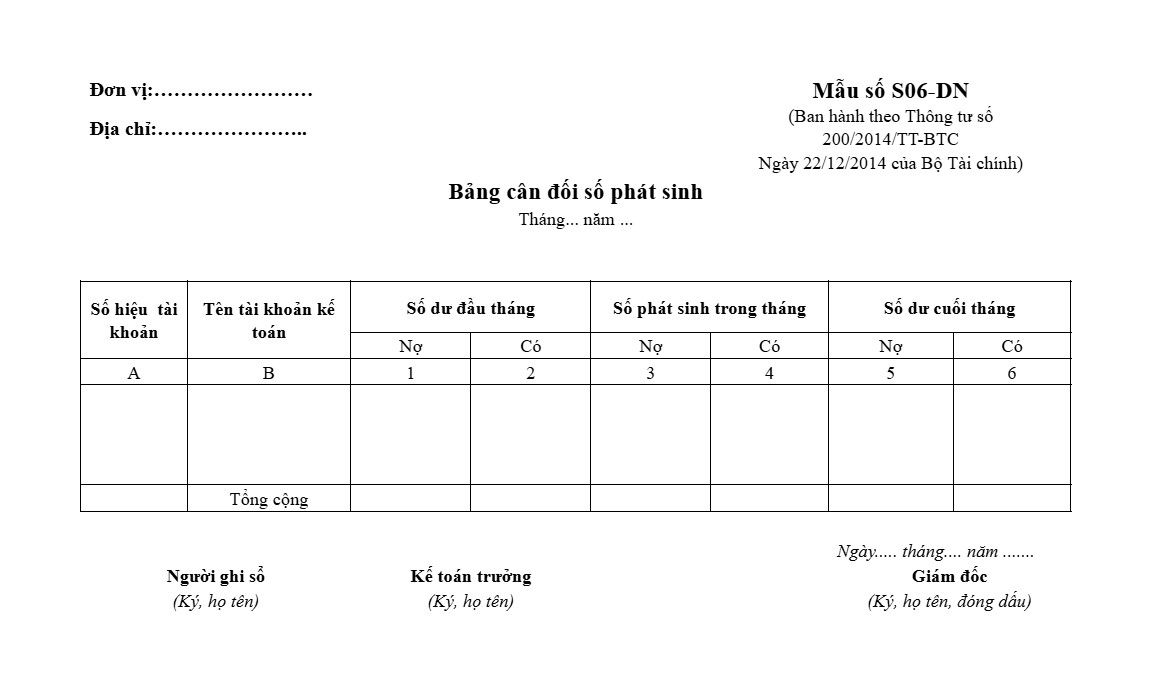

Sample trial balance according to Circular 200/2014/TT-BTC

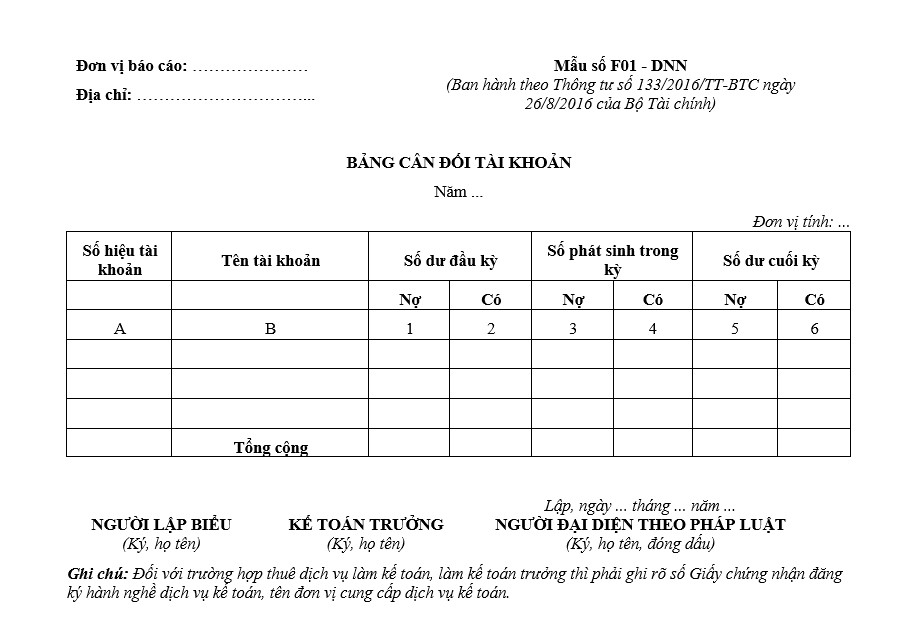

Sample trial balance according to Circular 133/2016/TT-BTC

| Download Template |

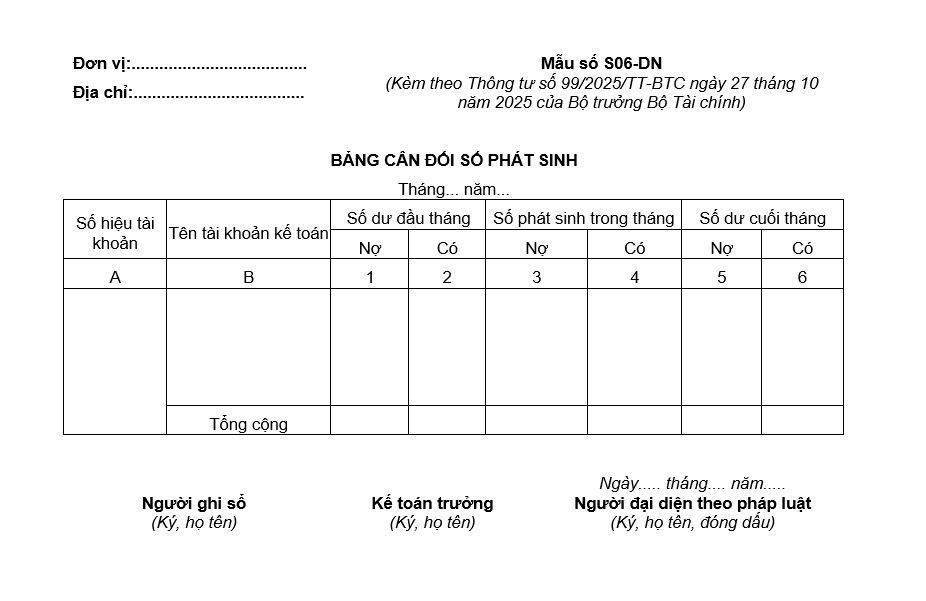

Sample trial balance according to Circular 99/2025/TT-BTC

| Download Template |

Instructions for checking and preparing the Trial Balance according to Circular 99/2025/TT-BTC

Appendix III attached to Circular 99/2025/TT-BTC provides instructions on filling out form S06-DN, the Trial Balance, as follows:

- The verification and preparation of the Trial Balance must be carried out on the basis of complete data from the General Ledger and the Trial Balance of the previous period to ensure the continuity and consistency of accounting data. This is a mandatory principle to avoid discrepancies between the opening balance and the closing balance of the period.

- Before conducting the audit and preparing the Trial Balance, accountants must complete all recording in the detailed and general ledgers. Simultaneously, they must perform a review and cross-checking between related ledgers (such as accounts payable, cash, inventory, etc.) to ensure the data is consistent, accurate, and reflects the true nature of the economic transactions. Only when the underlying data has been fully verified can the Trial Balance be considered valid as a basis for preparing financial statements.

The figures recorded in the Trial Balance are divided into two categories:

- The account balance figures reflect the status of each accounting account at the beginning of the period, as shown in columns 1 and 2, which are carried over from the end of the previous period. At the end of the period, as shown in columns 5 and 6, are the results after all changes during the period have been aggregated.

- The data on transactions during the period reflects all increases and decreases in each account from the beginning to the end of the reporting period. Transactions are shown in columns 3 and 4, where the total debit value of each account is recorded in the Debit column and the total credit value is recorded in the Credit column.

Below is the detailed structure of each column and the corresponding recording principles according to current regulations:

- Core A, B – Account Numbers and Names: Record the full code and name of all level 2 accounts that the business is using during the period. For more in-depth analysis, additional related level 2 accounts can be added for management and detailed control purposes.

- Columns 1 and 2 – Beginning Balance: Shows the balance at the beginning of the reporting period (i.e., the opening balance). The data to fill in these two columns is taken from the "Beginning Balance" line in the General Ledger for the first month of the period or the ending balance of the previous period's Trial Balance.

- Columns 3 and 4 – Transactions during the period: Reflect the total debit and credit transactions of each account throughout the reporting period. The data is compiled from the "Cumulative transactions from the beginning of the month" row of each corresponding account in the General Ledger.

- Columns 5 and 6 – Ending Balance: Shows the balance as of the last day of the reporting period. The data can be taken directly from the “Ending Balance” line in the Ending Ledger or calculated based on the beginning balance (columns 1 and 2) and transactions during the period (columns 3 and 4). This ending balance will be used as the basis for transferring to the beginning balance column of the next reporting period.

After filling in all the relevant data, A trial balance must be prepared, and the figures in the trial balance must meet the following mandatory balance requirements:

- Total Debit Balance (Column 1): Shows the total debit balance of all accounts at the beginning of the period, carried over from the previous period. This is the basis for checking the continuity of accounting data.

- Total Credit Balance (Column 2): Records the total opening credit balance of all accounts, ensuring a balance between debit and credit sides from the beginning of the accounting period.

- Total Debit Transactions (Column 3): Reflects the total value of economic transactions that increased the debit side during the period. This data is compiled from the general journal or ledger.

- Total Credit Transactions (Column 4): Shows the total value of transactions that increase the credit side during the period. In principle, total debit transactions must equal total credit transactions.

- Total Ending Debit Balance (Column 5): This is the remaining debit balance of the accounts after adding the beginning balance and adjusting for transactions during the period.

- Total Ending Credit Balance (Column 6): Reflects the remaining credit balance of accounts at the closing date, used as the basis for preparing financial statements.

Note: The trial balance not only summarizes the accounts on the balance sheet but also includes off-balance sheet accounts. This helps businesses fully track obligations, commitments, or internal management items that are not yet eligible for recognition as assets or liabilities.

The importance of checking and preparing the Trial Balance.

Overall assessment of the financial situation

By examining and preparing a trial balance, businesses can:

- Get a comprehensive overview of assets, liabilities, and equity.

- Track changes during the accounting period.

- Identify unusual upward or downward trends in costs, revenue, or accounts payable.

This is a crucial basis for managers to make appropriate and timely operational decisions.

Tools for checking the accuracy of accounting records.

The trial balance not only serves as a summary but also acts as an effective "error filter" in the accounting record-keeping process.

When checking each account, line by line, the mandatory principle is:

|

Ending balance = Beginning balance + Total increases – Total decreases |

If this equation is incorrect, it is highly likely that the following has happened:

- Accounting errors

- Missing or duplicate documents

- Formula error when aggregating data.

When checking the total flow, at the aggregate level, three principles of balance must be ensured:

- Beginning debit balance = Beginning credit balance

- Total debits = Total credits

- Total ending debit balance = Total ending credit balance

If any of these three conditions are broken, the accounting system definitely has a technical error.

Basis for preparing financial statements and operational analysis.

Data from the audit and trial balance preparation process serves as direct input for:

- Prepare a Balance Sheet

- Prepare a Business Performance Report

- Capital utilization efficiency analysis

- Performance evaluation

An inaccurate trial balance will lead to a chain reaction of discrepancies throughout the entire reporting system.

Software application in checking and preparing the Trial Balance.

The modern accounting software that MAN – Master Accountant Network uses automates the process of checking and preparing trial balances. The application of technology brings many benefits:

Standardize forms according to regulations.

The software provides a standardized accounting system and reporting system that complies with current accounting regulations, supporting accountants in conveniently recording and verifying data, and minimizing formal errors.

Reconciliation between summary and detailed accounts

The system is capable of:

- Compare the figures between level 1 accounts and lower-level accounts.

- Detecting discrepancies between the general ledger and the detailed ledger.

- Warning when data is out of sync.

This allows accountants to address discrepancies before preparing financial statements.

Automatic error warning

Modern accounting software can:

- Detecting discrepancies in accounting entries.

- Identifying duplicate documents

- Alerts for unusual account activity (e.g., expense accounts with ending balances).

These warnings help businesses make timely adjustments, reducing risks during tax settlement.

In summary, checking and preparing the Trial Balance is not only a mandatory operational step but also a foundation for protecting the accuracy of the entire financial reporting system. When this process is carried out systematically, combining accounting expertise and modern technology, businesses will significantly minimize the risk of errors, discrepancies in figures, and the pressure of the tax season.

At MAN – Master Accountant Network, we apply an integrated accounting software system with automated reconciliation technology and intelligent alerts to most of our clients. Automating the process of checking and preparing the Trial Balance shortens processing time, minimizes manual data entry errors, and ensures that data is always tightly controlled before financial reporting.

See more: Full accounting service

Conclude

Checking and preparing the Trial Balance is not simply a matter of compiling data, but a crucial control step to ensure the accuracy and transparency of the entire accounting system. When done correctly, combined with appropriate software tools, the Trial Balance becomes a solid foundation for effective financial reporting and business management.

If your business is looking for solutions to optimize accounting processes, reduce data verification pressure, and improve reporting reliability, MAN – Master Accountant Network is ready to partner with you to build a transparent, accurate, and sustainable financial system right from the ground up.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about Checking and Preparing the Trial Balance

According to Circular 99/2025, where should the revaluation of digital assets at the end of the period be accounted for?

The revaluation difference of digital assets (if there are specific guidelines on market price) is usually recorded in account 412 (Revaluation difference of assets) or accounts 515/635 depending on whether the asset is classified as an investment or an operating asset.

Do electronic trial balances need to be printed out on paper?

Not mandatory. According to Circular 99/2025/TT-BTC, electronic accounting records have the same legal validity as paper records if they ensure integrity and have a valid digital signature.