In the context of a constantly changing accounting legal framework and strong digital transformation, the accounting process for small and medium-sized enterprises (SMEs) is no longer simply about record-keeping but has become the foundation for financial management and risk control. This article provides a comprehensive, up-to-date, and practical overview of standard accounting processes for SMEs in 2026, from the latest legal basis and detailed 7-step implementation, to tax accounting, common mistakes, and accounting trends in 2026, helping businesses operate legally, maintain financial transparency, and optimize business efficiency.

The Importance of Standardized Accounting Practices in the Digital Age 2026

Entering 2026, the role of accountants in small and medium-sized enterprises (SMEs) has undergone a landmark change. Accounting is no longer simply about recording numbers in ledgers; it has become a strategic advisory role for business owners. A well-structured accounting process for SMEs helps to ensure transparency in cash flow, optimize tax costs, and provide timely data for investment decisions.

In particular, 2026 marks a significant transition in Vietnam's accounting legal framework. This is driven by the government's comprehensive digitalization efforts through electronic invoices generated from cash registers and new regulations. Circular 46/2025/TT-BTC This requires accountants to continuously update their skills in order to operate accounting processes in small and medium-sized enterprises as effectively as possible.

Criteria for defining SMEs in 2026

To properly apply accounting procedures for small and medium-sized enterprises (SMEs), businesses first need to determine their size category according to Decree 80/2021/ND-CP. This classification directly affects the accounting regime and accompanying tax incentives.

- Micro-enterprises: Revenue under 3 billion VND/year or the average number of employees contributing to social insurance per year does not exceed 10 people.

- Small businesses: Revenue under VND 50 billion/year or capital under VND 20 billion.

- Medium-sized enterprises: Revenue under VND 200 billion/year or capital under VND 100 billion.

Each type of business will have different requirements regarding the level of detail in the accounting process for small and medium-sized enterprises. However, if your business has foreign investment, you need to consult further. FDI enterprise accounting process To gain a thorough understanding of transfer pricing regulations and international financial reporting.

Accounting legal framework for SMEs

Currently, SMEs mainly operate according to the following regulations:

- Circular 133/2016/TT-BTC: This serves as a "guiding principle" for the current accounting process of small and medium-sized enterprises, helping to simplify the chart of accounts and reporting.

- Circular 46/2025/TT-BTC: Amending several provisions of Circular 133, effective from July 1, 2025, focusing on increasing the flexibility of document templates and promoting electronic accounting.

- Circular 99/2025/TT-BTC: The new accounting system will replace the old regulations from 2025; however, businesses need to prepare their data systems in 2026 to ensure a seamless transition.

After clearly identifying which SME category the business belongs to and the corresponding accounting regime according to current regulations, the next important issue is how to implement the accounting process for SMEs correctly, completely, and effectively in actual operation. Based on this legal foundation, businesses need a specific, systematic, and easy-to-apply process. The following section will delve into a detailed analysis of the standard accounting process for SMEs in 7 steps, helping accountants and business owners control the entire accounting lifecycle from documents to financial statements.

Detailed accounting procedures for small and medium-sized enterprises (SMEs).

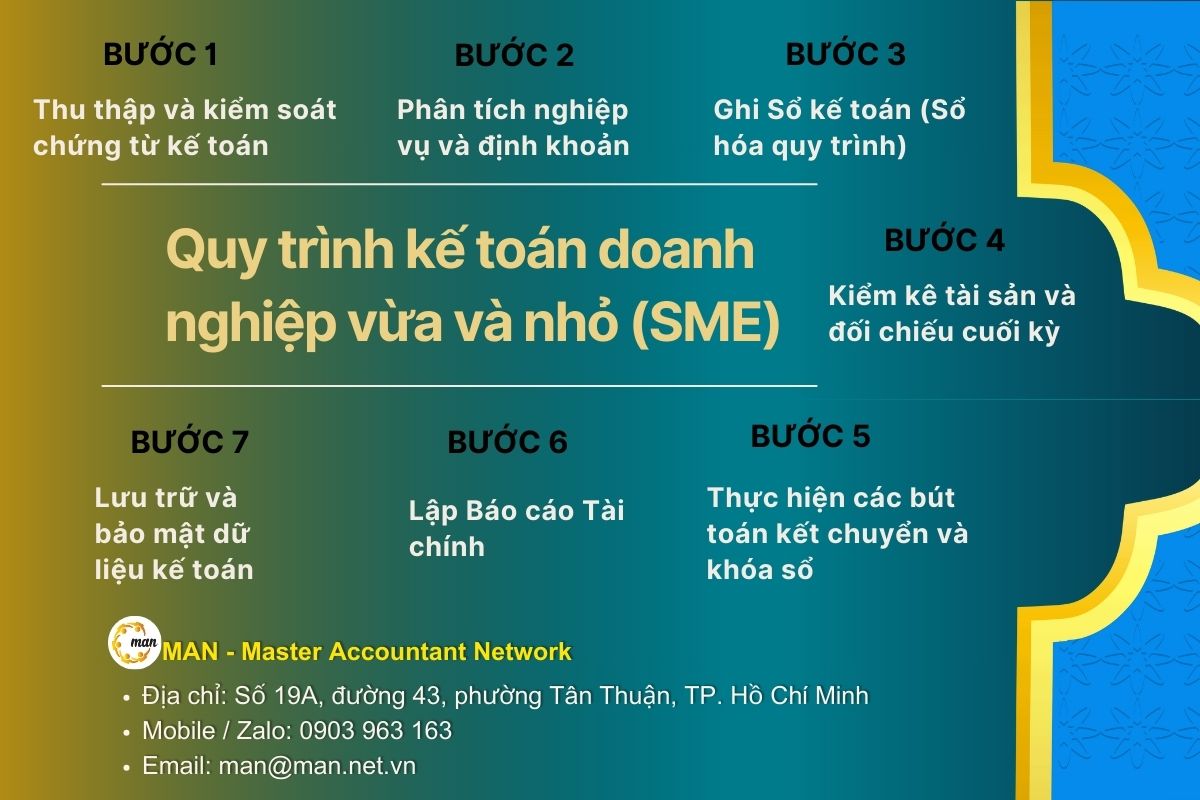

To build a solid accounting process for small and medium-sized enterprises, accountants need to strictly adhere to the following 7-step cycle:

Step 1: Collect and Control Accounting Documents

This is the most important starting point in the accounting process for small and medium-sized enterprises. Every economic transaction must be reflected through documentation.

- Input documents: Electronic invoice (verify validity on the General Department of Taxation's portal), warehouse receipt, handover record.

- Output documents: Sales invoices, delivery notes, economic contracts.

- New feature in 2025: According to Circular 46/2025/TT-BTC, businesses are allowed to design their own document templates, but they must ensure that they include all seven elements: Document name, number, date, name/address of the unit, transaction content, quantity/unit price/total amount, and signatures of the parties involved.

Step 2: Business Analysis and Journal Entry

After receiving valid documents, the accountant proceeds with the analysis to determine the corresponding accounts. In the accounting process for small and medium-sized enterprises according to Circular 133, the chart of accounts has been significantly streamlined.

- Businesses need to pay attention to accounts such as Account 111 (Cash), Account 112 (Bank Deposits), Account 152 (Raw Materials), Account 156 (Goods), and Account 642 (Business Administration Expenses).

- Making the correct accounting entries from the start helps to speed up the closing process at the end of the period.

Step 3: Record in the accounting books (Digitize the process)

In the 2026 era, accounting processes for small and medium-sized enterprises (SMEs) have largely shifted to software-based record-keeping. Common forms include:

- General log: Records all transactions in chronological order.

- General Ledger: Systematizes business transactions according to each accounting account.

- Detailed ledger: Tracks each individual debtor and each inventory item in detail. Software is used to automate the transfer of data from the journal to the general ledger, minimizing manual errors.

Step 4: Inventory and End-of-Period Reconciliation of Assets

A small and medium-sized enterprise accounting process that lacks an inventory check step can easily lead to inaccurate financial reporting.

- Conduct a daily or weekly cash inventory.

- Compare your bank account balance through your bank statement or passbook.

- Conduct regular inventory checks to address issues related to damaged or obsolete goods.

- Submit the reconciliation statement for accounts payable to customers (Account 131) and suppliers (Account 331).

Step 5: Perform closing entries and finalize the books.

At the end of the accounting period (month/quarter/year), accountants perform closing entries to determine the business results:

- Transfer revenue (Account 511) and other income (Account 711) to Account 911.

- Transfer expenses (Accounts 632, 642, 811) to Account 911.

- Calculating net profit and accounting for corporate income tax (Account 821). This is a crucial stage in the accounting process for small and medium-sized enterprises to ensure data is ready for financial reporting.

Step 6: Prepare Financial Statements

SMEs applying Circular 133 will prepare a set of financial statements including:

- Financial Statement Report (Form B01-DNN).

- Report on business performance (Form B02-DNN).

- Explanatory notes to the Financial Statements (Form B09-DNN).

- Balance Sheet (Form F01-DNN). In the accounting process for small and medium-sized enterprises, financial statements must be submitted to the Tax Authority, the Statistics Authority, and the business licensing authority within 90 days from the end of the fiscal year.

Step 7: Storing and Securing Accounting Data

At the end of each accounting cycle for small and medium-sized enterprises, records must be stored systematically.

- Documents used for management and administration: Must be retained for a minimum of 5 years.

- Documents used for accounting entries and financial statement preparation: Must be retained for a minimum of 10 years.

- With the cloud trends of 2026, businesses should back up their data on cloud computing platforms with two-factor authentication to avoid the risk of data loss.

Thus, fully implementing the 7 steps in the accounting process for small and medium-sized enterprises (SMEs) helps businesses tightly control documents, books, and financial data, while creating a solid foundation for preparing transparent and standardized financial reports. However, for the accounting process to be truly effective and to minimize legal risks, businesses cannot separate tax accounting from the overall accounting system. The following section will focus on analyzing tax accounting in SMEs in 2026, clarifying key taxes, declaration and settlement schedules, and important notes to help businesses comply with regulations and optimize tax obligations legally.

Tax accounting in SMEs

Tax accounting is an integral part of the accounting process for small and medium-sized enterprises (SMEs). Businesses need to pay particular attention to the following:

Basic and preferential tax rates

Within the accounting process for small and medium-sized enterprises (SMEs), understanding basic tax regulations and applicable preferential policies is a prerequisite for accurate tax declarations, minimizing the risk of tax arrears, and optimizing legal tax obligations. Specifically, the taxes that SMEs need to pay particular attention to include:

- VAT: Most SMEs choose the deduction method (tax rate 10%, some industries are reduced to 8% under support policies).

- Corporate Income Tax: The standard tax rate is 20%. However, micro-enterprises may be eligible for lower preferential tax rates to encourage production and business activities.

- Personal income tax: Filing should be done monthly (if the tax liability is large) or quarterly, and an annual tax settlement must be completed for all employees.

Although the regulations on tax accounting for SMEs are relatively clearly guided by law, in reality, not all businesses apply them correctly and fully during implementation. The discrepancy between the regulations on paper and their practical application in daily operations has led to many SMEs facing tax and accounting risks. Based on these real-world situations, the following section of MAN – Master Accountant Network will summarize practical implementation experiences and common mistakes that SMEs often encounter, helping businesses proactively prevent and improve their accounting processes.

Common mistakes in the accounting process of small and medium-sized enterprises.

In practice, even with accounting procedures established in accordance with regulations, many SMEs still make mistakes due to ingrained management habits, lack of internal control, or failure to keep up with new legal requirements. These errors not only affect the accuracy of financial reports but also pose significant risks during tax settlements and audits. The table below summarizes common errors that SMEs frequently encounter in practice, along with their consequences, to help businesses proactively review and prevent them.

| Error | Reality | Consequences |

| Invalid invoice | The accountant did not check the seller's operating status; nor did they look up the tax identification number before recording the input invoice. | The risks include using "phantom" invoices, having expenses disallowed during tax settlement, and facing back taxes and administrative penalties. |

| Confusing personal expenses and business expenses. | Business owners use company cards for personal expenses; accountants fail to separate expenses that are not related to business operations. | Expenses that are not accepted when calculating corporate income tax can distort profits and increase the risk of tax audits. |

| Incorrect or incomplete cost accounting | For service businesses, the costs are not fully recorded in account 154; the cost of goods sold is not accurately recorded. | Inaccurate business performance reports can easily raise suspicions and lead to in-depth audits by tax authorities. |

If the accounting process of small and medium-sized enterprises (SMEs) is not tightly controlled from the documentation and accounting stages to the aggregation of expenses, businesses are very likely to face the risk of expense disallowances, tax arrears, and prolonged audits. Regular review, standardization of processes, and timely updating of new regulations are key factors in helping SMEs minimize errors and enhance financial transparency in the long term.

SME accounting trends in 2026

The accounting processes of small and medium-sized enterprises are facing major technological changes:

- AI applications: Artificial intelligence can now automatically read data from PDF invoices and suggest appropriate accounting entries. This helps reduce manual data entry time.

- Green accounting (ESG): Banks are beginning to prioritize lending to SMEs with transparent financial reporting and indicators of environmental and social compliance. This is a new element that needs to be integrated into modern accounting processes for small and medium-sized enterprises.

- Preparing for Circular 99/2025/TT-BTC: Businesses need to review their accounting systems to prepare for the change in asset and liability classification according to internationally recognized standards in 2026.

Conclude

In the context of constantly changing accounting and tax regulations and increasing demands for financial transparency, building and operating a systematic accounting process for small and medium-sized enterprises (SMEs) not only helps businesses comply with regulations but also serves as a foundation for cost control, tax risk mitigation, and improved management efficiency. A standardized accounting process, updated according to new regulations and utilizing appropriate technology, will help SMEs be more proactive in tax audits and inspections, and ready for the next stage of development.

If your business is struggling to standardize accounting processes, update to new regulations, or needs to review its accounting systems before the tax season, partnering with MAN – Master Accountant Network – a specialized accounting, tax, and financial consulting firm, will be a safe and effective solution. Our team of experienced experts will help your business accurately assess its current situation, optimize processes, and ensure sustainable legal compliance, allowing you to focus on your core business activities.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder and CEO of MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

MAN Editorial Board – Master Accountant Network