During the process of establishing, dissolving, or converting a business type, determining the conditions for consolidating financial statements for a tax period is crucial for businesses to reduce paperwork burden and avoid penalties. This article analyzes all legal regulations under Circular 78/2014/TT-BTC, clarifying the scope of application, implementation procedures, and common errors encountered in accounting practice. Through this, businesses and accountants can confidently apply the regulations correctly, optimize tax obligations, and ensure transparent and legally sound tax settlement documents.

How is the corporate income tax period determined?

Before delving into the conditions for consolidating financial statements for tax periods, we need to clearly understand the concept of "Tax Period" as defined by current law.

According to Clause 2, Article 3 of Circular 78/2014/TT-BTC, the corporate income tax (CIT) calculation period is determined as follows:

- According to the Gregorian calendar: From January 1st to December 31st each year. This is the most popular choice for businesses in Vietnam.

- According to the fiscal year: In cases where a business is permitted by the competent authority to use a fiscal year different from the calendar year (for example, starting on April 1st and ending on March 31st of the following year), the tax period will be based on that fiscal year.

- First and last tax periods: For newly established businesses or cases of transformation (type, form of ownership), merger, division, dissolution, bankruptcy, the tax period is determined in accordance with the accounting period as prescribed by accounting law.

Correctly identifying the tax period is a crucial step in determining whether a business is eligible to apply for consolidation of financial statements for tax periods.

Details of the conditions for requesting consolidation of financial statements for the corporate income tax period.

According to Clause 3, Article 3 of Circular 78/2014/TT-BTC, the law allows businesses to combine the first or last tax year with the next/previous period if they meet strict time requirements.

Entities permitted to combine tax periods

The regulations regarding the consolidation of tax periods do not apply to all cases of normal operation, but focus only on specific entities, as follows:

- Newly established businesses: From the date of issuance of the Business Registration Certificate or Investment Certificate.

- Businesses undergoing restructuring or ceasing operations: This includes changing the type of business, changing the form of ownership, merging, acquiring, splitting, separating, dissolving, or going bankrupt.

Conditions for requesting consolidation of financial statements for tax periods shorter than 3 months.

This is the requirement for consolidating financial statements for the prerequisite tax period. Specifically:

- For newly established businesses: If the first tax period (from the date of licensing to the end of the fiscal/calendar year) is shorter than 3 months, the business is entitled to combine it with the tax period of the following year.

- For businesses undergoing dissolution or transformation. (Type of business, change of ownership form, merger, acquisition, division, separation, dissolution, bankruptcy)If the final tax period (from the start of the fiscal year to the date of the dissolution/conversion decision) is shorter than 3 months, the enterprise is entitled to combine it with the tax period of the previous year.

Conditions for requesting consolidation of financial statements for a tax period not exceeding 15 months.

After satisfying the condition of less than 3 months, the business needs to check the upper limit condition. The total duration of the tax period after consolidation (consolidation period) must absolutely not exceed 15 months.

If the total period exceeds 15 months, even if the first or last period is shorter than 3 months, the business must still file separate tax return reports for each period. This is an extremely important point to note when applying for consolidation of financial statements for tax periods.

A practical example of tax period consolidation.

To better understand how the conditions for consolidating financial statements for a tax period apply, let's look at the following two cases:

Case 1: Newly established business

Company A was granted its Business Registration Certificate on October 15, 2024. Due to the application of the calendar year tax period, the first tax period of 2023 for Company A is calculated from October 15, 2024 to December 31, 2025 (approximately 2.5 months).

- Eligibility criteria: Less than 3 months.

- Total estimated combined time: 2.5 months (2024) + 12 months (2025) = 14.5 months.

- Conclusion: Not exceeding 15 months. Company A is eligible to apply for consolidation of its 2024 tax year financial statements into the 2025 tax year.

Case 2: Business dissolution

Company B operates on a calendar year basis. Due to economic difficulties, Company B is undergoing dissolution procedures and has officially ceased operations on February 20, 2025. The final tax period (2025) is from January 1, 2025 to February 20, 2025.

- Eligibility criteria: Less than 3 months.

- Total estimated combined time: 12 months (2024) + 1.7 months (2025) = 13.7 months.

- Conclusion: Not more than 15 months. Company B is eligible to apply to consolidate its financial statements for the 2025 tax year with those for the 2024 tax year. However, since the 2024 tax year is usually due (before March 31, 2025), Company B needs to notify the tax authorities early.

Procedures for requesting the consolidation of corporate income tax periods and financial statements.

Although Circular 78/2014/TT-BTC clearly stipulates the right to consolidate, in terms of administrative implementation, businesses need to pay attention to the following steps to ensure transparency.

Is it necessary to submit a written request for permission?

In principle, if a business fully meets the conditions for consolidating financial statements for a tax period, it has the right to do so on its own. However, in practice, the electronic tax system (Etax) usually defaults to one tax period per year. Therefore, to avoid being flagged for outstanding tax returns or late payment penalties, businesses should draft a notification letter regarding the consolidation of tax periods and send it to the directly managing Tax Office/Tax Department.

Deadline for submitting applications after merger

The deadline for submitting the letter requesting the consolidation of financial statements and corporate income tax returns is before the deadline for submitting the financial statements for the year for which consolidation is requested.

For example: Company X requests to consolidate its 2025 financial statements into those of 2026; the deadline for submission is March 31, 2026.

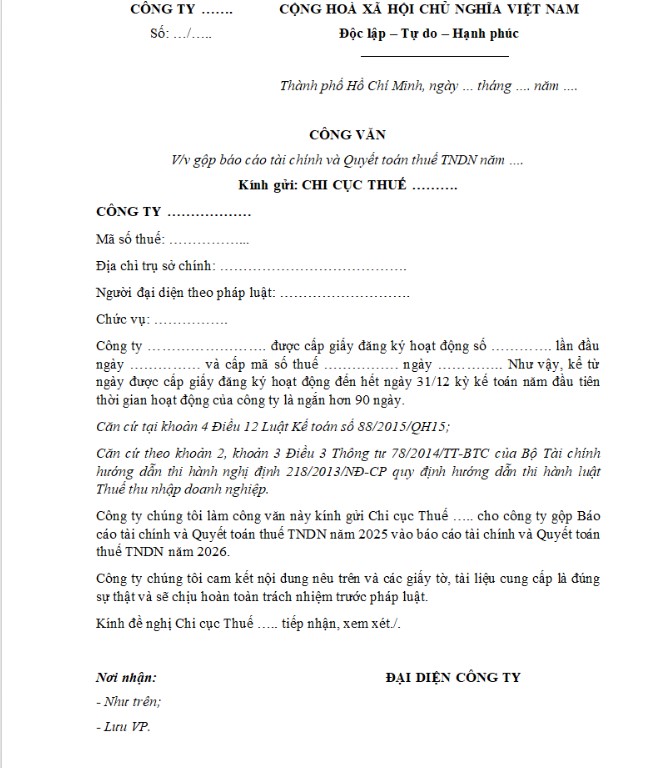

Sample letter requesting consolidation of financial statements.

Based on current legal regulations, not all businesses have the right to arbitrarily combine accounting periods. This is only permitted when the conditions regarding the length of operation in the first year are met.

The benefits of businesses being eligible to consolidate financial statements for tax periods.

Consolidating tax periods offers several practical benefits for business management:

- Reduced paperwork burden: Instead of preparing two sets of financial statements and tax returns, businesses only need to prepare one set.

- Optimize tax payments: Offset losses from the first few months against the following year's income immediately.

- Cost savings on audits: This is especially beneficial for FDI businesses that are required to undergo annual audits.

Common mistakes when consolidating tax periods

Despite being fully aware of the requirements for consolidating financial statements for a tax period, many accountants still make mistakes such as:

- Forget the 15-month condition: If the company's fiscal year differs from the calendar year, the cumulative total could exceed 15 months if not carefully calculated.

- Failure to notify the tax authorities will result in the tax return being pending in the tax management system.

- Errors in invoice consolidation: Omitting documents generated during the "odd months" of the previous year when preparing consolidated reports.

Understanding the requirements for consolidating financial statements for a tax period helps accountants be more proactive in organizing documents and optimizing benefits for the business.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about the conditions for requesting consolidation of financial statements for tax periods.

Can a business that has been established for exactly 3 months combine its tax periods?

No. According to Clause 3, Article 3 of Circular 78/2014/TT-BTC, the mandatory condition is that the first or last tax period must be "shorter than 3 months". If a business is established between October 1st and December 31st (exactly 3 months), it does not meet the conditions for consolidation and must still prepare a separate tax return for that period.

Is it mandatory for businesses to submit a formal request to combine tax periods?

Legally, businesses are not required to apply for permission if they meet the conditions for consolidating financial statements for a tax period. However, in practice, for tax management purposes, businesses should proactively send a notification letter to the tax authority to: avoid being flagged as missing declarations by the eTax system, avoid penalties for late filing of tax returns, and facilitate explanations and tax audits/inspections.

Is it permissible to combine tax periods but not financial statements?

It is not advisable for businesses to combine corporate income tax periods while still preparing separate financial statements for each year: The tax settlement figures will not match the financial statements, causing significant difficulties for tax authorities during verification, and increasing the risk of tax assessment or requests for further explanations.

Can FDI enterprises apply for the condition of consolidating financial statements for tax periods?

Yes. Domestic businesses or foreign-invested enterprises (FDI). The requirements are: They must be in the correct category (newly established, dissolved, converted, merged, etc.), the tax period must be shorter than 3 months, and the total period after consolidation must not exceed 15 months. FDI enterprises are fully permitted to consolidate periods and can significantly reduce audit costs for short-term periods.

MAN Editorial Board – Master Accountant Network