In the context of the digital economy and the groundbreaking changes to the amended Personal Income Tax Law of 2026, mastering the process of declaring personal income tax on the Tax Declaration Support Software (HTKK) has become more important than ever for all accountants. With the new family allowance deductions approved by the National Assembly, the indicators on the Tax Declaration Support Software (HTKK) have also been adjusted accordingly.

This article was prepared in consultation with senior tax and accounting experts to help you file your tax returns accurately and avoid unnecessary administrative penalties.

Overview of changes in personal income tax policy.

Before delving into the instructions for filing personal income tax returns on the HTKK system, we need to review the core changes that will take effect from the 2026 tax year:

Personal allowance deductions:

- For the taxpayer themselves: Increased to VND 15.5 million/month (instead of VND 11 million as in the previous period).

- For each dependent: Increase to VND 6.2 million/month (instead of VND 4.4 million).

The progressive tax system involves slight adjustments to the spacing between tax brackets to reduce the burden on middle-income workers.

Data requirements: The General Department of Taxation has begun fully implementing personal identification numbers as tax identification numbers, requiring extremely accurate input data on the HTKK system.

Should personal income tax returns be filed monthly or quarterly?

Whether a business files its personal income tax return monthly or quarterly depends on the value-added tax (VAT) filing period it is currently applying.

According to the provisions of Articles 8 and 9 of Decree 126/2020/ND-CP, the principle for determining the declaration period is implemented as follows:

Monthly declaration

Businesses must file personal income tax returns monthly if they are eligible to file VAT returns monthly. If a business does not meet the conditions for quarterly VAT filing, it is automatically required to file personal income tax returns monthly.

Quarterly declaration

Businesses are allowed to file personal income tax returns quarterly if they meet the conditions for quarterly VAT filing, meaning their total revenue in the preceding year was 50 billion VND or less. Additionally, businesses have the right to choose the quarterly filing method, but must determine and apply it from the first quarter in which the tax filing obligation arises.

Therefore, businesses must proactively determine whether they are required to file monthly or quarterly tax returns based on their revenue and actual conditions. After choosing a filing method, businesses need to maintain that method consistently throughout the calendar year.

Instructions for filing personal income tax returns quarterly on the HTKK system.

To be ready to file your tax return, please download and install the latest version of the HTKK software.

Here are the detailed instructions on how to fill out the quarterly personal income tax return (Form 05/KK-TNCN according to Circular 80/2021/TT-BTC) using the latest HTKK software:

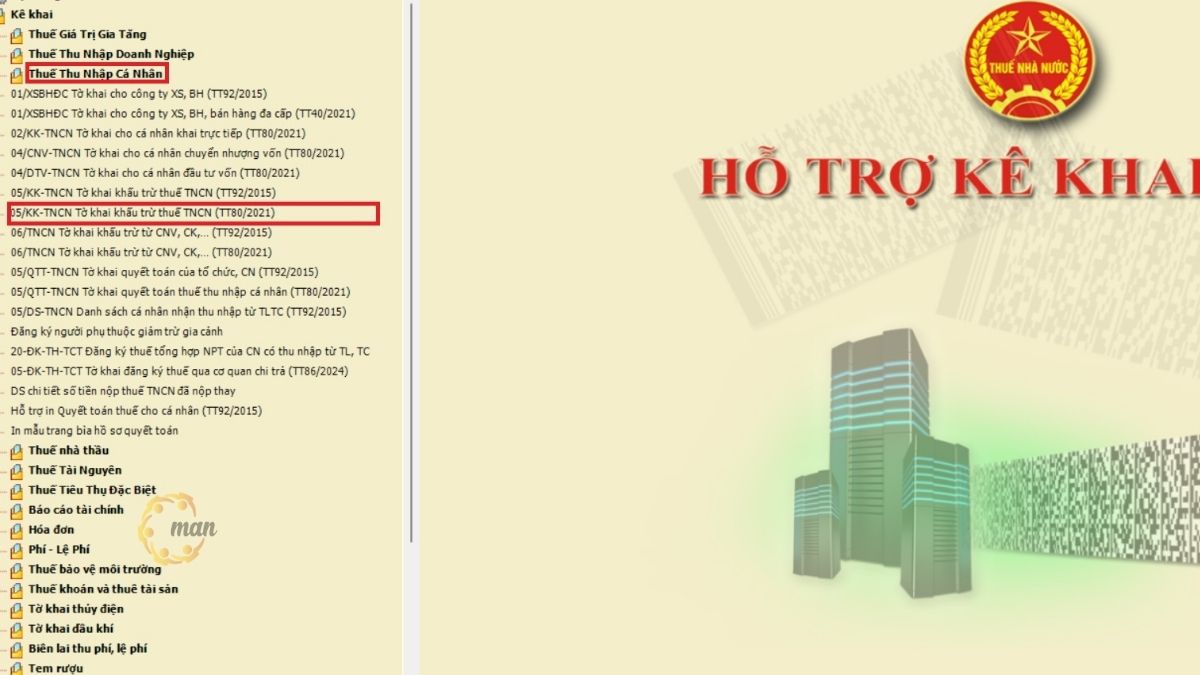

Step 1 – Log in to HTKK

Log in to the latest version of the HTKK system using the tax identification number (TIN) of your registered business.

Step 2 – Select the quarterly personal income tax deduction form.

To select the quarterly personal income tax withholding declaration form: Click on "Personal Income Tax", then select the correct form "05/KK-TNCN Personal Income Tax Withholding Declaration Form (Circular 80/2021)".

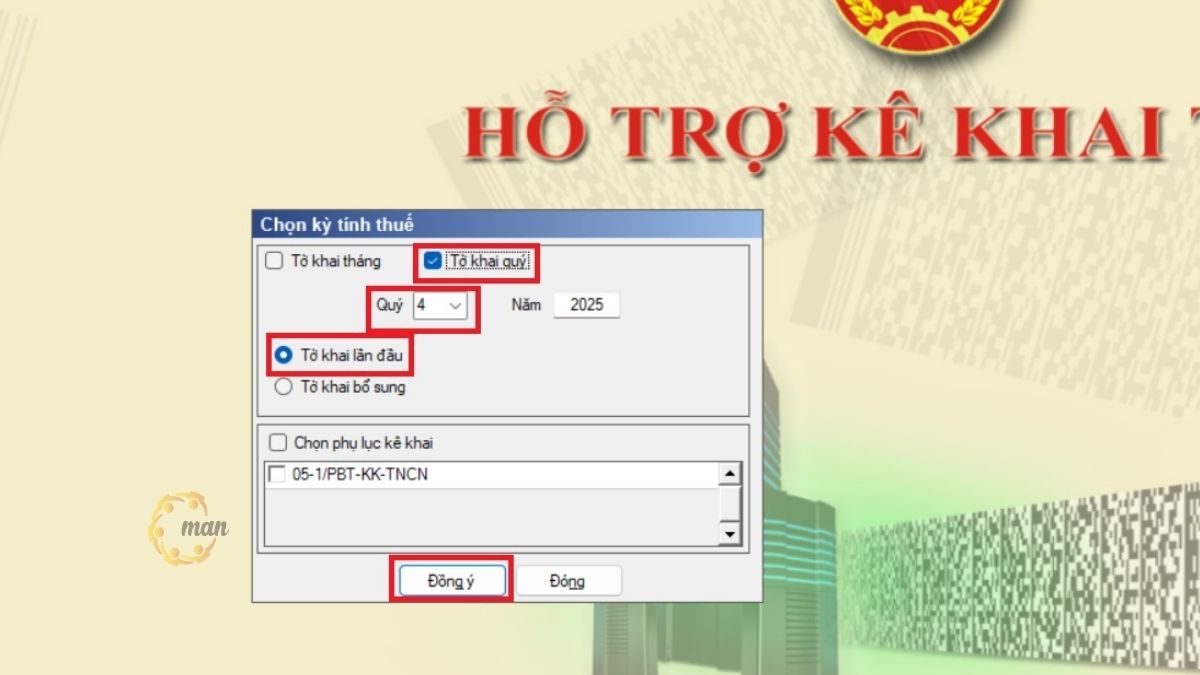

Step 3 – Select quarterly filing period

Next, select "Quarterly Filing Period", click to select the first filing, and then click "Agree".

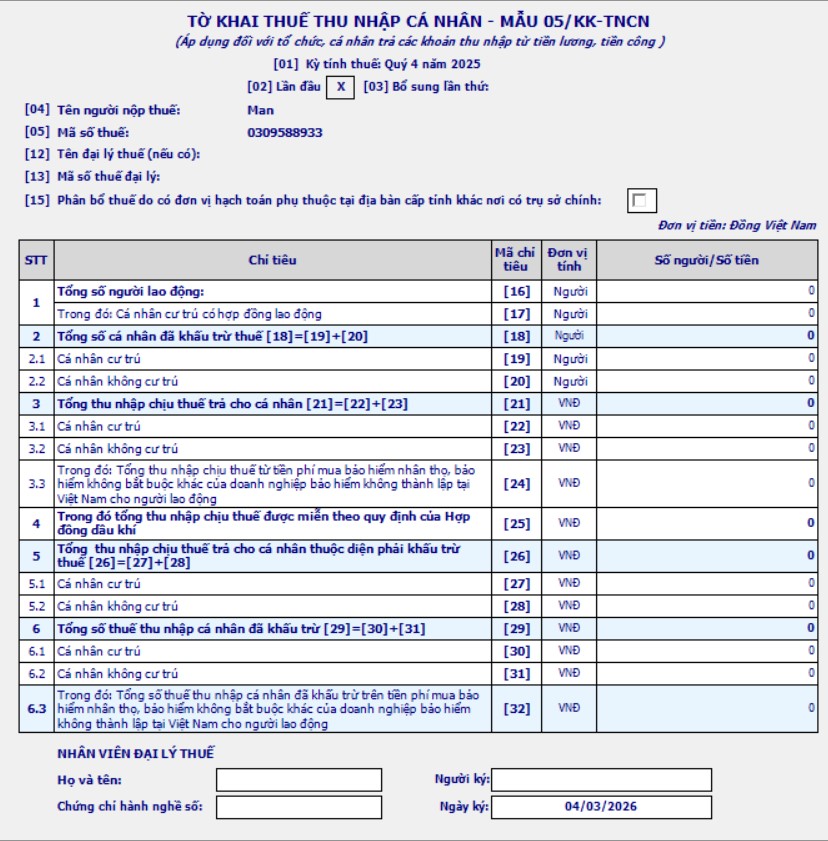

Step 4 – Fill in the details of the items on the quarterly personal income tax return.

When preparing the Personal Income Tax Return using form 05/KK-TNCN, accountants need to pay special attention to the following key indicators to ensure that the declared data is accurate, complete, and in accordance with regulations.

Here are the details on how to fill in the fields:

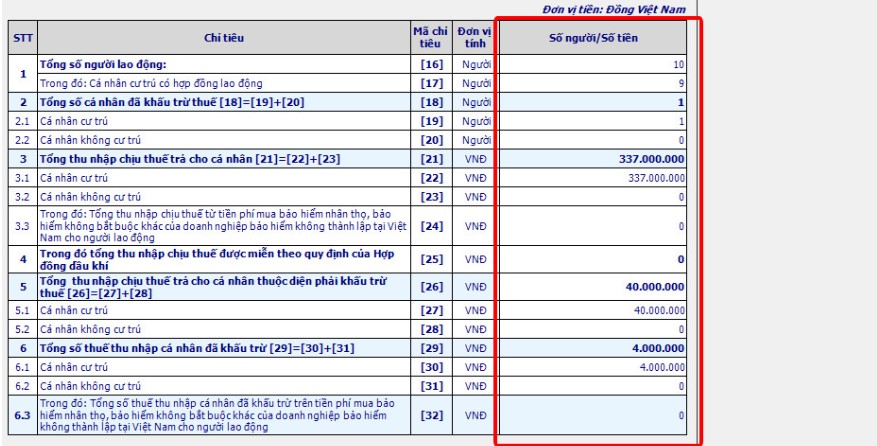

- Indicator [16] Total number of employees: Is the total number of individuals who generate income from salaries and wages paid by organizations and individuals during the declaration period.

- Indicator [17] Resident individuals with labor contracts: Is the total number of resident individuals who have signed labor contracts for 03 months or more and receive salary and wage income from the paying unit during the period.

Note: The data at indicator [16] must be greater than or equal to (≥) the number recorded at indicator [17].

- Indicator [18] Total number of individuals whose tax has been deducted: Determined by formula [18] = [19] + [20]. The declaration support software will automatically calculate and update this indicator.

- Indicator [19] Resident individuals: Reflects the number of resident individuals whose income from salaries and wages has been subject to personal income tax withholding during the period. The accountant records the number of resident workers for whom the enterprise has withheld tax when paying income.

- Indicator [20] Non-resident individuals: Shows the number of non-resident individuals whose salary and wage income has been tax-deducted by the paying unit during the declaration period.

- Indicator [21] Total taxable income paid to individuals: Determined by formula [21] = [22] + [23]. Data is automatically compiled by the software.

- Indicator [22] – Resident individuals: Includes all taxable income from salaries, wages and similar payments made to resident individuals during the period.

- Indicator [23] – Non-resident individuals: Is the total taxable income from salaries, wages and similar payments that the unit has paid to non-resident individuals during the period.

- Indicator [26] Total taxable income paid to individuals subject to tax withholding: Determined by formula [26] = [27] + [28]. The software will automatically update the corresponding data.

- Indicator [27] – Resident individuals: Reflects taxable income from salaries, wages and income of a salary or wage nature paid to resident individuals subject to tax withholding as prescribed in the declaration period.

Note:

- The data recorded in indicator [27] must always be less than or equal to (≤) the data in indicator [22].

- Indicator [22] – Total taxable income: Reflects the total taxable income of all employees during the period, regardless of whether there is any tax payable or not.

- Indicator [27] – Total taxable income of individuals subject to tax: Only includes the taxable income of workers subject to personal income tax obligations. Therefore, the value in this indicator cannot be greater than the total taxable income recorded in indicator [22].

- Indicator [28] – Non-resident individuals: Shows taxable income from salaries, wages and similar payments that the paying unit has paid to non-resident individuals and are subject to tax withholding in the declaration period.

- Indicator [29] – Total amount of deducted personal income tax: Determined by the formula: [29] = [30] + [31]

This information is usually automatically compiled by the software system.

- Indicator [30] – Resident individuals: Record the total amount of personal income tax that organizations and individuals paying income have deducted from resident individuals in the period. This is the amount of tax deducted from the income of resident workers in the declared quarter/month.

- Indicator [31] – Non-resident individuals: Reflects the amount of personal income tax withheld from the income of non-resident individuals during the period.

Step 5 – Save the declaration and export the XML file

After entering the data into the HTKK declaration form, click "Save," then select "Export XML" to export the saved file in XML format.

Step 6 – Log in to the online tax website to submit your tax return.

Log in to the electronic tax website (https://thuedientu.gdt.gov.vn/etaxnnt/RequestEnter your business name and password, then submit it like any other tax return.

Prepare a supplementary personal income tax return using the HTKK system.

If, after submitting your quarterly personal income tax withholding return and it is officially accepted, you discover errors that require correction, you should prepare a supplementary tax return. Here are the details on how to prepare it:

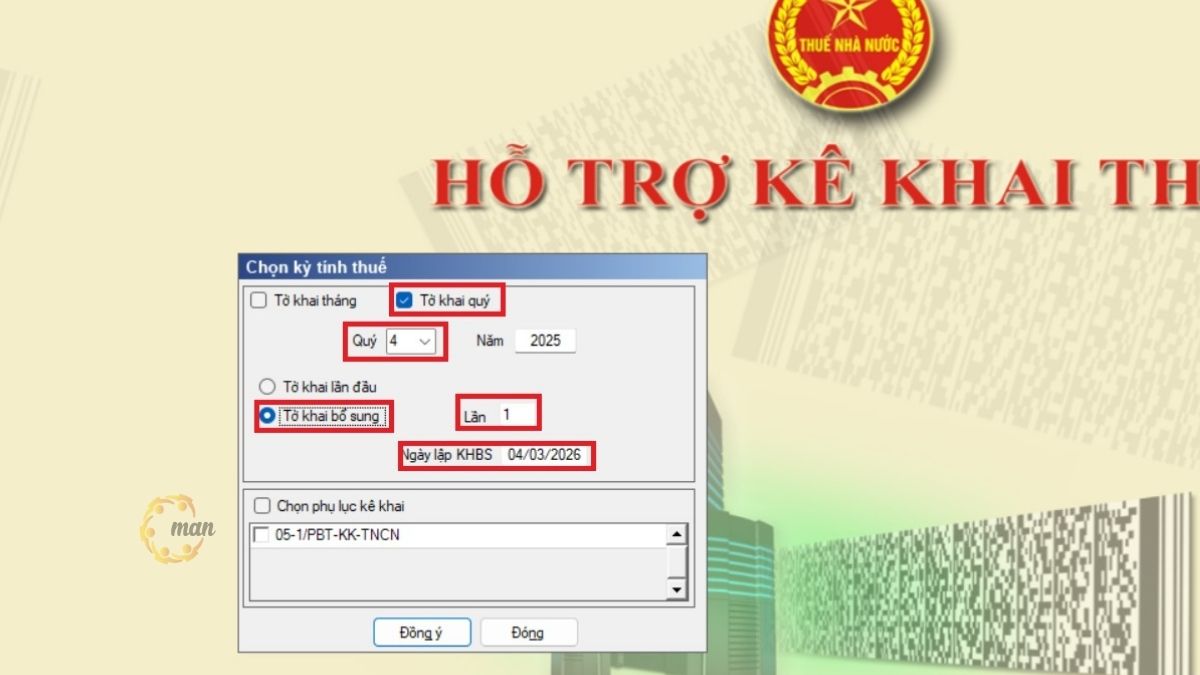

Step 1 – Log in and select the supplementary personal income tax filing period.

Perform the login process as you did the first time, but when you reach the step to select the tax filing period and filing number, select "Add to tax return" and click "Agree".

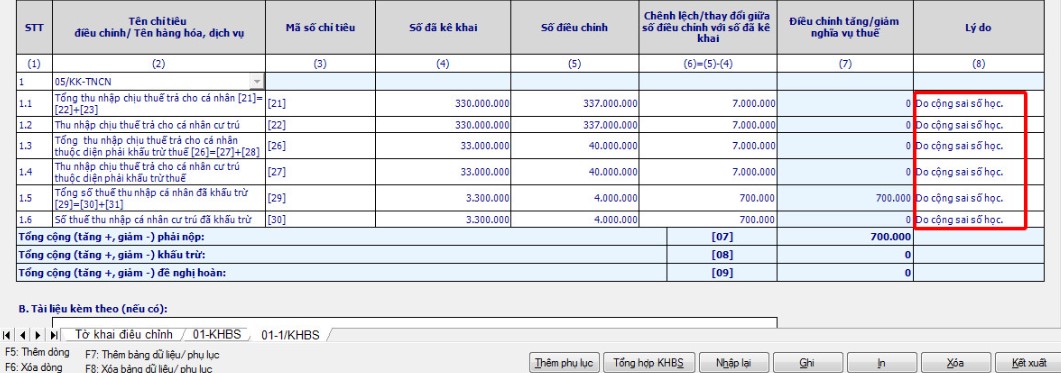

Step 2 – Correct the erroneous entries on the supplementary declaration form.

The accountant reviews and updates any inaccurate declarations directly on the supplementary declaration form. After completing the adjustments, select the "Save" function to save the information, and the system will automatically compile the data into appendices 01/KHBS and 01-1/KHBS as required.

Step 3: Enter the information into supplementary declaration form 01/KHBS

Carefully check the electronic transaction code of the first accepted personal income tax return, then enter it in the electronic transaction code field.

Items 1, 2, 3, and 4: Calculated automatically by the software.

Step 4 – Fill in the explanatory information in Appendix 01-1/KHBS

Provide a reason or explanation for each adjusted item.

Step 5 – Export the XML file and submit the personal income tax return.

After entering all the information, click "Save," then select "Export" to create an XML file for online submission, just like other tax returns on the website. https://thuedientu.gdt.gov.vn/etaxnnt/Request.

Deadline for submitting tax returns when filing personal income tax returns on HTKK software.

When filing personal income tax returns on the HTKK system, businesses and individuals paying income should pay special attention to the deadline for submitting documents to avoid administrative penalties for tax violations.

According to the Law on Tax Administration 38/2019/QH14 (Article 44), the deadline for submitting tax returns is stipulated as follows:

- Monthly tax filing: The deadline is no later than the 20th day of the month following the month in which the tax liability arises (for example, the deadline for filing the tax return for February 2026 is no later than March 20, 2026).

- Quarterly tax filing: The deadline for filing and paying taxes quarterly is the last day of the first month of the quarter following the quarter in which the tax liability arises. (If the filing date falls on a public holiday, the filing will be done on the next working day after the holiday).

Correctly identifying the filing period (monthly or quarterly) will help ensure accurate personal income tax declarations on the HTKK system and minimize errors.

Deadline for paying personal income tax

The deadline for paying personal income tax coincides with the deadline for filing the tax return for the corresponding period.

In case of errors requiring supplementary declaration, according to Clause 1, Article 55 of the Tax Administration Law 38/2019/QH14, the deadline for paying the tax difference is the deadline for submitting the tax return for the adjusted tax period.

Important notes when filling out the form:

- If errors are discovered in the settlement, the paying entity must prepare a supplementary declaration form 05/KK-TNCN for each month or quarter with errors, and simultaneously make adjustments using the HTKK software.

- Only organizations and individuals that make payments of salaries and wages are required to file personal income tax returns.

In cases where no payments are made during the period, a tax return for that month or quarter does not need to be submitted, as stipulated in Decree 126/2020/ND-CP and guided by Official Letter 2393/TCT-DNNCN.

Understanding these deadlines and principles will help businesses file personal income tax returns on the HTKK system correctly, avoiding the risk of late payment penalties or tax arrears.

Conclude

Understanding the deadlines for filing tax returns and paying taxes is crucial for ensuring accurate and compliant personal income tax declarations on the HTKK system, minimizing the risk of penalties. Even a few days' delay or incorrect declaration of the tax period can lead to unnecessary fines and late payment penalties.

Therefore, in addition to closely monitoring the deadlines stipulated in the Tax Administration Law 38/2019/QH14, businesses should proactively review payroll and wage data and conduct reconciliation before submitting tax returns on the system.

If you need assistance with document review, error checking, or detailed advice on the personal income tax declaration and settlement process, please refer to: professional tax settlement services Contact MAN – Master Accountant Network immediately for specific guidance, ensuring compliance with the law and optimizing tax costs safely and effectively.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.