Maintaining a journal is a fundamental accounting practice, but it also carries significant legal risks if done incorrectly, especially in the context of 2026 when electronic invoices, digital documents, and tax data connectivity become mandatory requirements. This article provides comprehensive guidance, from the latest legal basis and principles of "standard, complete, and correct" journal entries to technical skills and common errors, helping accountants, businesses, and household businesses maintain journal entries correctly, transparently, and be prepared for any tax audits or inspections.

The importance of keeping a journal.

With the digital economy booming, journal entries are no longer simply a matter of static data storage. They have become a crucial business process, acting as a "transfer station" for data from disparate electronic documents into the overall financial management system of a business. To understand why this practice holds a top priority in modern accounting, we need to consider its conceptual aspects, strategic role, and the technological shifts in the near future.

What is a journal?

The Journal is a general accounting book used to record economic and financial transactions that occur during each accounting period (month, quarter, year) in chronological order. It is the "journal" that records all changes in the unit's assets and capital before these figures are compiled into the General Ledger.

Strategic role

Recording entries in the Journal is crucial in the accounting system because:

- Data foundation: This is the sole basis for entering data into the General Ledger and preparing the Trial Balance. If this step is incorrect, the entire financial report will lose its accuracy.

- Tax transparency: Ensuring transparency helps businesses easily explain their financial situation to tax authorities during audits.

- Legal evidence: In civil or economic disputes, a properly maintained logbook is the most important evidence confirming the transactions that have been completed.

By 2026, the shift to electronic documents and invoices generated from cash registers will have become widespread. Journal entries will no longer be purely handwritten but will require real-time data connectivity, ensuring continuous updating (Real-time accounting).

Mandatory legal regulations

For entries in the Journal to be legally valid, accountants must comply with the following regulations:

- Accounting Law No. 88/2015/QH13: Regulations on the principles of honesty, objectivity, and accounting procedures.

- Circular 200/2014/TT-BTC: Applicable to businesses in all sectors and economic components (especially large businesses).

- Circular 133/2016/TT-BTC: Accounting regime for small and medium-sized enterprises.

- Circular 99/2025/TT-BTC: Guidance on the accounting regime for enterprises.

However, mastering the new legal regulations is only a necessary condition. To apply them correctly and effectively in practice, accountants need to clearly understand each form of journal entry permitted by law, and then choose the method that suits the scale, specifics of operations, and accounting organizational structure of the unit.

Distinguish between different forms of journal entry.

Depending on the size and accounting method, businesses can choose one of the following approaches:

General Journal format

This is the most common method currently in use. All transactions are recorded in the General Journal in chronological order.

- Advantages: Simple, easy to track events in real time.

- Disadvantage: For large businesses, the ledger can be too long, making it difficult to categorize by account manually.

Journal – Ledger format

Combine journal entries and ledger entries in the same book.

- Features: Suitable only for small businesses with few operations.

- Structure: One side shows the chronological order, the other side divides the columns according to the main accounts.

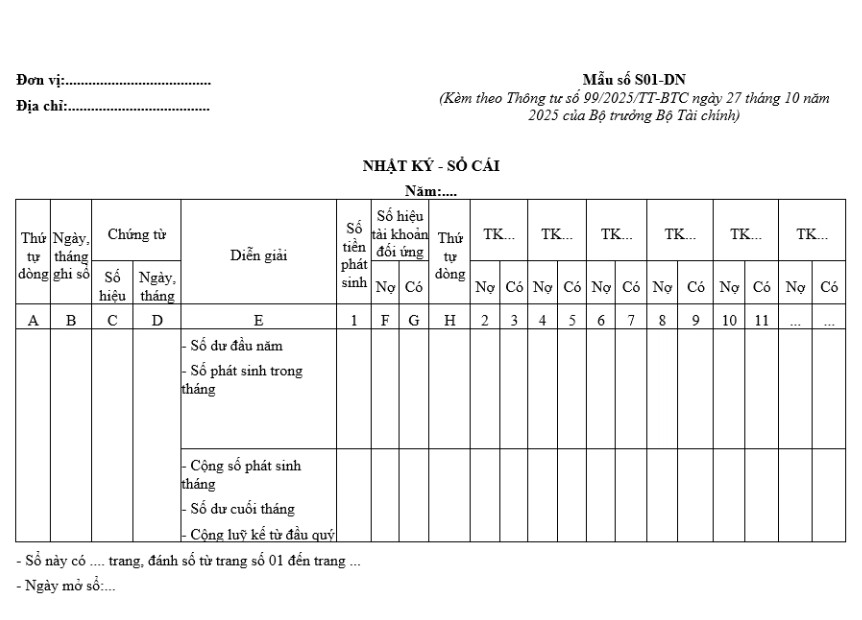

Sample Journal and Ledger according to Circular 99/2025/TT-BTC

Structure and principles of recording in the Journal and Ledger according to Circular 99/2025

Structure

The Journal-Ledger is an integrated general accounting book designed to combine the chronological recording function of a journal with the data systematization function of a ledger.

Diary section

The Journal section is responsible for recording all economic transactions that occur in the Journal Book, arranged continuously in chronological order to ensure the completeness, continuity, and comparability of accounting data.

The entries in the Journal include the following columns:

- Column “Date of entry”

- Column “Number”

- Column “Date of the document”

- Column “Explanation” (business content)

- Column “Amount incurred”

General Ledger Section

The General Ledger is designed for each specific accounting account, with each account tracked separately using two columns reflecting the direction of change: Debit and Credit. Depending on the scope of operations and the number of accounts used at the unit, the structure of the ledger can be expanded or reduced accordingly. Through recording in the Journal and transferring data to the General Ledger, economic transactions are summarized and clearly classified according to the economic nature of each account, creating a basis for preparing accurate and transparent financial statements.

Principles of recording entries in the Journal

Daily recording: Recording in the Journal must be done regularly and continuously as soon as accounting documents arise. Before recording, the person in charge of the Journal and Ledger is responsible for reviewing the legality and validity of the documents. Based on the economic content reflected, the accountant conducts transaction analysis and accurately determines the debit and credit accounts according to accounting principles.

In cases where multiple documents of the same nature arise, accountants can first consolidate them using a Summary Table of Accounting Documents of the Same Type. Based on this, the essential information for recording in the Journal (or Journal-Ledger) will be reflected in a centralized, complete, and systematic manner, instead of recording each document individually.

When recording entries in the Journal, each accounting voucher or summary of similar vouchers is reflected on a single line in the Journal-Ledger system. This entry simultaneously reflects information from both sections: the Journal section, which reflects the chronological order of the transaction, and the Ledger section, which tracks the corresponding relationships between accounting accounts. This recording method ensures data consistency and facilitates reconciliation and aggregation of data at the end of the period.

Record the following entries in the Journal:

- Column “Date of entry”

- Column “Number”

- The "Date" column of the document

- The "Explanation" column (details of the business transaction)

The "Amount Amount" column (based on the amount recorded on the document)

General Ledger Section: The amount of each economic transaction is reflected correspondingly in the Debit and Credit sides of the relevant accounts according to the accounting correspondence, specifically as follows:

- Columns F and G: Record the corresponding account numbers for the economic transaction;

- Column H: Record the sequential number of the transaction in the Journal - Ledger;

- From column 2 onwards: Record the amount generated for each account according to the corresponding accounting entries already recorded in columns F and G.

At the end of the accounting month, the accountant must summarize all transactions recorded in the journal, separately determining the total debits and credits, and the balance of each account. Based on this, they then accumulate the total transactions from the beginning of the quarter, which serves as the basis for preparing and reconciling the indicators on the financial statements.

See more: Business accounting process

Conclude

Maintaining a journal is not only a mandatory requirement under accounting regulations but also a crucial foundation for the quality of an entity's entire accounting system and financial reports. In the context of 2026, when tax authorities strengthen electronic data management and automated reconciliation, accurate, timely, and proper record-keeping becomes more important than ever. Accountants, businesses, and household businesses need to proactively update their knowledge of new legal regulations, choose appropriate record-keeping methods, and apply technology to minimize the risk of errors. A well-maintained and transparent journal not only helps businesses comply with the law but also provides a solid foundation for effective financial management and peace of mind during tax audits and inspections.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about Journal Entry

Is a signature required in a journal?

Yes. Accounting ledgers must be signed by the person who prepared the ledger, the chief accountant (or person in charge of accounting), and the legal representative as prescribed. For electronic ledgers, digital signatures are accepted if they meet legal requirements.

Do small businesses need to keep complete records in a journal?

For business households paying taxes using the declaration method, maintaining accounting records, including the prescribed journal, is mandatory from 2026 according to Circular 152/2025/TT-BTC, regardless of revenue size.

What should be done if errors are discovered after the books have been closed?

Once the books are closed, accountants are not allowed to make direct corrections but must make adjustments through accounting entries in the next period, while clearly explaining the reasons and effects of the adjustments in the financial statements.

How long is a journal entry kept on file?

According to the Accounting Law, accounting records must be stored for a minimum of 10 years. For electronic data, businesses must ensure that it is accessible, readable, and printable when requested by competent authorities.