Accounting practices in the General Ledger and Sub-ledgers for businesses from 2026 onwards must fully comply with the updated regulations in Circular 99/2025/TT-BTC – the new legal document completely replacing Circular 200/2014/TT-BTC on the accounting regime for businesses. Circular 99/2025/TT-BTC, effective from January 1, 2026, expands the scope of application, increases autonomy in designing accounting and reporting systems, and provides a more aligned approach with IFRS and digital technology in accounting record-keeping in general. Therefore, a thorough understanding of the principles and techniques of recording in the General Ledger and Sub-ledgers according to the new legal framework will help accountants ensure accuracy, transparency, and legal compliance in all transactions.

What is a ledger?

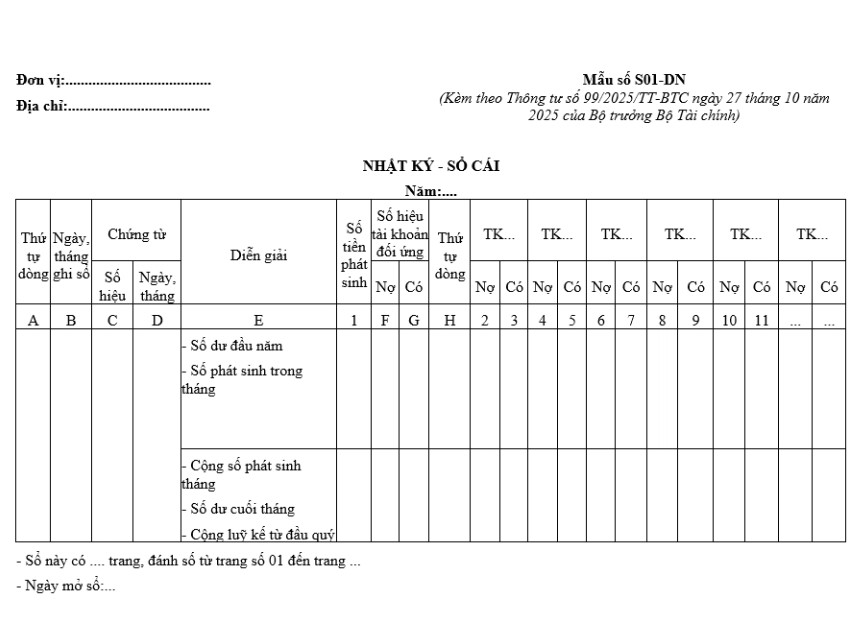

The general ledger is a comprehensive accounting book used to record all economic and financial transactions that occur during a period, categorized by accounting account. It provides an overall picture of a company's assets, capital, revenue, expenses, and business results.

According to Circular 99/2025/TT-BTC (effective from January 1, 2026), the General Ledger is a mandatory part of a company's accounting system and must be fully and continuously recorded, and reconciled with the subsidiary ledgers.

The main purpose of keeping a ledger.

In fact, the ledger is not simply a place to record data, but also performs many important functions such as the following:

- Recording all financial changes in detail: The general ledger's function is to reflect all economic transactions occurring within the business in chronological order. From buying and selling goods, incurring expenses, and generating revenue to settling accounts payable, borrowing, or other liabilities, everything is systematically documented in corresponding accounting accounts.

- Clearly showing the status of each account: Each account in the accounting system has its own tracking section in the General Ledger, allowing businesses to see the specific amounts of money increased, decreased, and the remaining balance. This ensures transparency in income and expenses and the sources of asset formation, minimizing confusion and errors in financial management.

- The basis for comparing and verifying data: The general ledger serves as the foundational data source for reviewing and verifying the accuracy of accounting information. When it is necessary to retrieve a past transaction or for inspection, auditing, or tax settlement purposes, the general ledger is a crucial document for verifying data and assessing the level of compliance with legal regulations.

The Role of the Ledger

The role of the ledger is:

- Summarize all changes in each account.

- This serves as the basis for preparing the Trial Balance.

- It serves as the basis for preparing financial statements.

- It is an important document when auditing and settling taxes.

Note: If the General Ledger is wrong, the entire Financial Statement will be wrong.

What is a ledger?

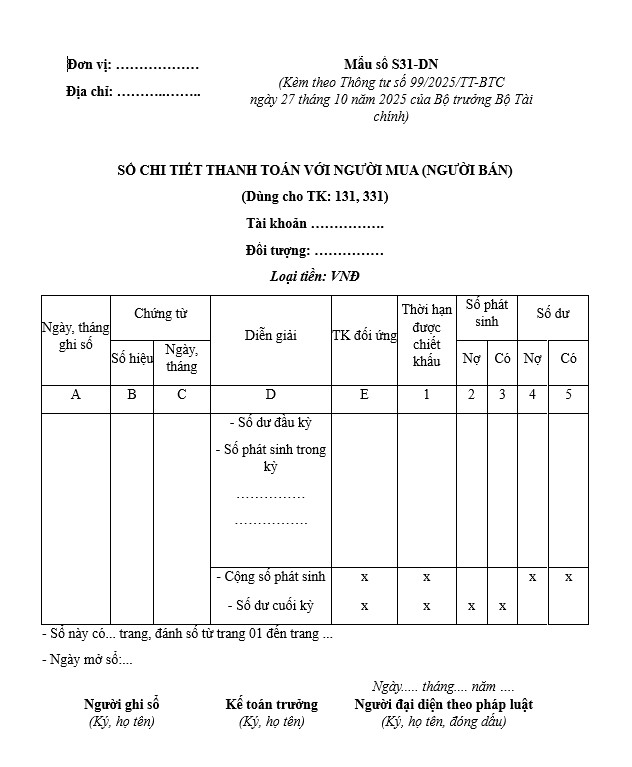

Detailed ledgers (detailed accounting ledgers) are a type of accounting ledger used to record in detail the economic and financial transactions related to a specific accounting object (assets, capital, revenue, expenses) for internal management purposes, which the General Ledger cannot fully reflect. The data in the detailed ledgers is used for comparison with the General Ledger and other functional departments.

The main purpose of recording in the ledger.

The main purpose of recording in the detailed ledger is:

- Providing detailed information for each transaction: The detailed ledger fully records every transaction that occurs for each accounting object. Each line clearly shows the time of execution, the content of the transaction, the debit and credit values, and related data, making it easy for users to trace back each item when needed for verification.

- Supporting reconciliation and ensuring accounting balance: By separately tracking each item, the detailed ledger helps accountants verify the consistency between transactions. This is an important basis for confirming that the total debit and credit transactions are accurately and consistently reflected in the summary ledger.

- Providing a foundation for analysis and reporting: Data from detailed ledgers serves as input for compiling and analyzing accounts receivable, inventory, expenses, or revenue by specific groups. This allows businesses to build financial and management reports with a higher level of detail, supporting decision-making.

The main role of the Ledger in the accounting system.

Detailed accounting ledgers play a crucial role in analyzing and controlling each accounting item in depth, helping businesses manage their finances more transparently and accurately. According to the accounting ledger organization principles in Circular 99/2025/TT-BTC, opening and maintaining detailed ledgers is mandatory to ensure comparability with the general ledger and to prepare accurate financial statements.

Here are the most important roles of the Ledger:

Manage accounts receivable by individual customer.

Detailed ledgers help businesses track specific information:

- How much does each customer still owe?

- How much does each supplier need to pay?

- Payment terms for each installment

This allows businesses to control cash flow and limit the risk of bad debt.

Asset and inventory control

For accounts such as supplies, goods, and fixed assets, the detailed ledger shows:

- Quantity of goods imported, exported, and in stock.

- The remaining value of each asset

- Specific usage conditions

This is especially important in cost management and end-of-period inventory.

The basis for comparison with the General Ledger.

The detailed ledger serves as the foundation for preparing the detailed summary statement. The total balance of all items in the detailed ledger must match the balance in the general ledger for the same account.

Without a detailed ledger, businesses would find it difficult to detect errors or discrepancies in data.

Support for tax inspection, auditing, and settlement.

When tax authorities, auditors, or management request an explanation of a specific item, the detailed ledger is the document that clearly demonstrates the transaction history and balance of each item.

Improving financial management efficiency

In addition to serving legal compliance purposes, the detailed ledger also helps managers:

- Evaluate the effectiveness of each customer.

- Cost analysis by department

- Track asset price movements over time.

See more: Should you hire a professional accounting firm or an in-house accountant?

The core differences between a General Ledger and a Detailed Ledger

To properly record entries in the General Ledger and Sub-ledgers, accountants first need to clearly distinguish the characteristics of each type:

Key features of the Ledger

The general ledger serves as a comprehensive overview and is the basis for preparing financial statements.

- Systematic nature: The ledger compiles data from all transaction journals, classifying them according to accounting accounts (from type 1 to type 9).

- High legal validity: The figures in the General Ledger must match the Trial Balance perfectly. This is the first set of documents the tax authorities examine during tax settlement.

- Form of expression: Reflected solely in monetary value. No detailed quantitative information such as quantity or quality specifications of goods is recorded.

- Frequency of recording: Depending on the accounting method (General Journal or Journal Voucher), the ledger is recorded daily or periodically on a monthly basis.

Key features of the Detail Ledger

The detailed ledger serves the purpose of internal management and closely monitoring even the smallest changes in the subject.

- Specificity: Reflects details for each entity (For example: Instead of just knowing the total debt of account 131, the detailed ledger shows how much Company A owes and how much Company B owes).

- Diversity of measurement units: In addition to monetary units, the detailed ledger flexibly uses physical units (kg, m, piece) and labor time units (work unit, hour).

- Timeliness: Transactions are typically recorded immediately after they occur, based on original documents, to facilitate immediate inventory control or accounts receivable management.

- Unlimited quantity: Businesses can have as many pages/accounts as they need to manage.

To avoid confusion during the recording process in the General Ledger and Sub-ledgers, accountants need to clarify the differences between them in many aspects such as purpose, subjects tracked, and basis for recording. The table below helps to systematize the core differences in a visual and easy-to-understand way.

| Criteria | Ledger | Detailed ledger |

| Purpose | It is used to summarize all financial transactions arising within a business, from daily transactions to large-value transactions such as investments and asset purchases. This is an important basis for preparing financial statements and evaluating the overall financial situation. | This allows for in-depth monitoring of each specific item within an account. It helps businesses analyze in detail the situation of accounts receivable, inventory, assets, etc., by customer, supplier, or individual item. |

| Structure | Typically, each account has its own page or section, including basic columns such as the entry date, transaction details, corresponding account, and debit/credit amounts. The design is comprehensive, not focusing on each specific item. | Organized by account type, each page or section displays detailed information on every transaction related to that type, enabling more specific and accurate tracking. |

| Layout | Transactions can be arranged by account order or chronological order. Different transactions within the same account are recorded consecutively on the same page. | They are divided into separate groups or categories. For example, each customer or supplier has its own tracking section, making it easier to search and manage. |

| Tracking range | It encompasses all of the company's financial activities at an aggregate level. | Focus only on specific items or objects within a given account. |

| Level of detail | Only record the key elements of the transaction, such as the date, content, related account, and amount. Do not reflect the details of each individual or entity involved. | This provides a more complete and specific representation, including detailed information on each transaction for each individual, customer, supplier, or specific asset. This allows for in-depth analysis of the transaction history and balances for each entity. |

Note: The total balance and transactions in the detailed ledgers of the same account must always equal the figures shown in the general ledger of that account. This is the basis for verifying the accuracy of the data.

See more: Hire an accounting service.

Reconciling the General Ledger and Sub-ledgers: A vital verification step.

Maintaining the General Ledger and Subsidiary Ledgers is meaningless if the figures between the two types of ledgers don't match. This is the most important internal control step.

Create a detailed summary table.

To verify the accuracy of the records, at the end of the accounting period, it is necessary to consolidate the data from all the detailed ledgers. This process is as follows:

- Object grouping: Accountants list all specific objects being tracked (e.g., individual customers, individual suppliers, or individual warehouses).

- Data output: Finalize the ending balance for each individual ledger page.

- Summary: Fill these values into a general spreadsheet (Detailed Summary Table).

Example: Suppose you are recording entries in the General Ledger and Sub-Lecturer for account 131 (Accounts Receivable). On the individual subsidiary ledgers:

- Company A: Outstanding debt of 10 million VND.

- Company B: Outstanding debt of 20 million VND.

- Company C: Outstanding debt of 5 million VND.

The total on the Summary Statement is 35 million VND. This figure of 35 million is the target for comparison with the General Ledger in the next step.

Match with the Ledger

Take the total from the Summary Table and compare it with the ending balance in the General Ledger Account 131.

- If they match: The entries in the General Ledger and Sub-Lecturer for the period have been correct.

- If there is a discrepancy: This could be due to duplicate entries, omissions, or errors in the data aggregation process.

The combination of these two types of ledgers creates a perfect double reconciliation system. Without a scientific approach to recording in the General Ledger and the Sub-ledgers, businesses can easily fall into situations of asset loss, discrepancies in accounts payable, and face significant risks during tax settlement.

Reference: Full accounting service

Conclude

In summary, the General Ledger and the Sub-ledger do not exist separately but always work together according to the principle of "synthesis - analysis". While the General Ledger helps businesses see the overall financial picture, the Sub-ledger provides the necessary depth to control each specific item. Organizing and recording these two types of ledgers in a coordinated manner not only ensures the accuracy of accounting data but also forms a crucial foundation for preparing financial statements, tax returns, and for audits and inspections.

If you are building or reviewing your business's accounting system, don't overlook standardizing the General Ledger and Sub-ledger recording process from the outset. Contact MAN – Master Accountant Network for detailed advice and support.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.