Filing corporate income tax returns is one of the most important obligations that businesses must fulfill correctly, completely, and promptly to avoid the risk of tax arrears and penalties from the tax authorities. With increasingly stringent requirements from the tax authorities, businesses need to clearly understand the regulations, master the necessary documents and records, and apply the correct filing process. This article provides an in-depth, easy-to-understand, and practical perspective to help you file corporate income tax returns effectively, transparently, and in accordance with regulations.

Overview of Corporate Income Tax Filing According to Standards

Corporate income tax declaration is the process by which businesses determine the amount of corporate income tax they must pay to the state budget, based on their business performance during the tax period.

What is corporate income tax filing? Who are the taxpayers?

Corporate income tax declaration is the process by which businesses compile, determine, and report the amount of tax payable to the State based on their business performance during the period. This is a mandatory obligation, carried out through provisional and annual tax returns, to ensure financial transparency and compliance with tax laws. Taxpayers include:

- Businesses established under Vietnamese law (Limited Liability Companies, Joint Stock Companies, etc.).

- Foreign organizations with or without a permanent establishment in Vietnam but with income generated in Vietnam (usually paying taxes using the withholding method or a percentage of revenue).

To file accurately, businesses need to understand the tax period and the tax calculation method. These two factors directly determine the amount of tax payable in each period.

Tax period and tax calculation method

The corporate income tax period is determined by the calendar year (from January 1st to December 31st) or the fiscal year (if the business registers a different accounting period). The main method for declaring corporate income tax is the revenue-expense method. Taxable income is determined by subtracting deductible expenses from revenue, then multiplying by the corporate income tax rate.

The corporate income tax filing process includes two main parts:

- Quarterly Provisional Corporate Income Tax Filing: During the fiscal year, businesses file provisional corporate income tax returns quarterly (no later than the 30th of the first month of the following quarter), but are NOT required to submit the tax return form. Businesses only need to pay the provisional tax amount (if any) to the state budget.

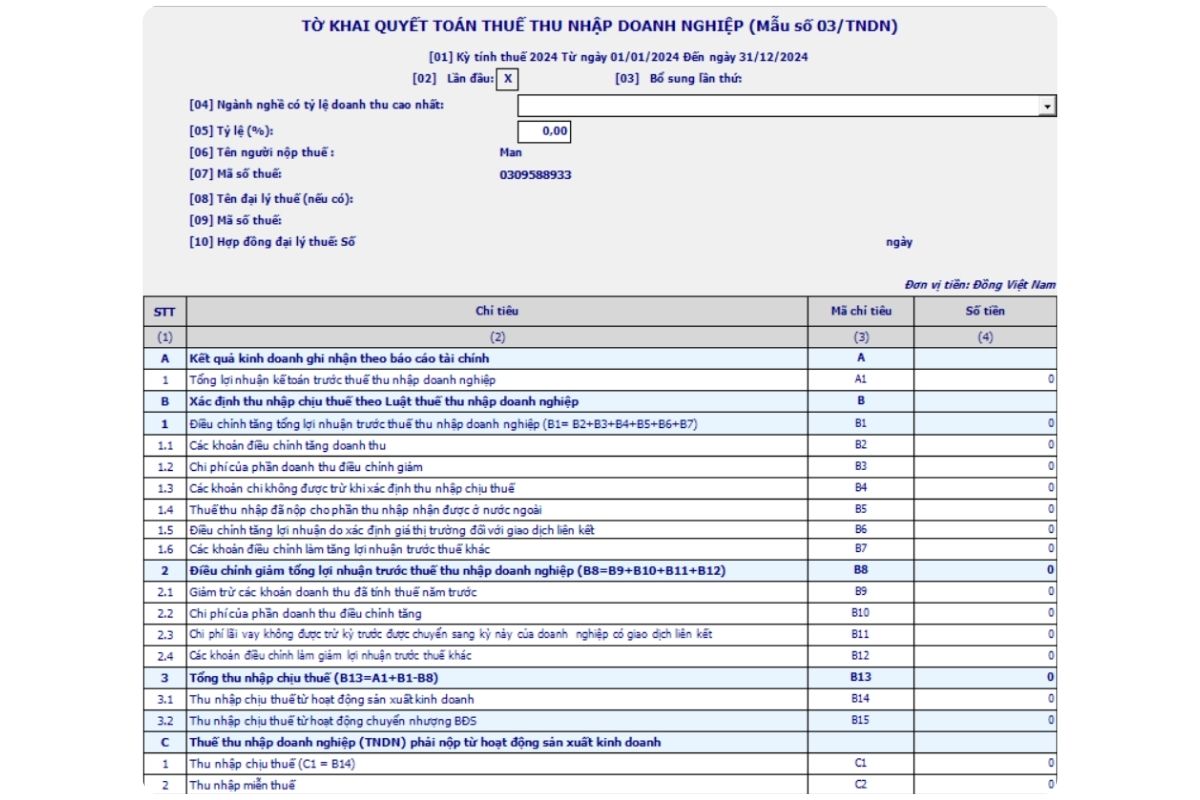

- Annual Tax Settlement: Businesses are required to submit the Annual Corporate Income Tax Settlement Declaration Form (Form 03/TNDN) along with the Financial Statements at the end of the fiscal year.

After thoroughly understanding the entire corporate income tax declaration process and the steps businesses need to take in each stage, the next step is to firmly grasp the legal basis that underlies this entire process. This helps businesses declare correctly according to regulations, minimize errors, and ensure transparency when working with tax authorities.

The legal framework governing corporate income tax declarations.

Corporate income tax declarations must strictly comply with the following legal regulations to ensure legitimacy.

| Document | Content | Applying corporate income tax declaration |

| Tax Law | Corporate Income Tax Law 2025 (No. 67/2025/QH15): Regulations on taxable subjects, income, expenses, tax rates, and incentives. | The basis for determining the tax base. |

| Management Law | Law on Tax Administration No. 38/2019/QH14: Regulations on tax administrative procedures, deadlines for submitting documents, and handling violations. | The framework regarding the procedures and deadlines for filing corporate income tax returns. |

| Decree | Decree 126/2020/ND-CP regulates quarterly provisional payments and settlement responsibilities. | Basis for determining the obligation to make provisional payments over four quarters. |

| Circular | Circular No. 80/2021/TT-BTC: Guidance on the implementation of the Law on Tax Administration, including the declaration form (Form 03/TNDN). | The basis for preparing the Corporate Income Tax return and submitting it via the HTKK system. |

| Anti-Transfer Pricing | Decree No. 132/2020/ND-CP: Regulations on related-party transactions. | Mandatory for businesses with linked transactions. |

Based on the aforementioned legal documents, businesses can fully identify the grounds for filing corporate income tax returns correctly, ensuring transparency, compliance, and minimizing risks when working with the Tax Authority.

Update on the most important new points regarding corporate income tax declaration.

The Corporate Income Tax Law of 2025 introduces many important changes that directly affect the calculation and declaration of corporate income tax for businesses from 2025 onwards.

Changes to Corporate Income Tax Rates

Businesses need to be aware of changes in tax rates, especially new preferential rates, which have a significant impact on the amount of corporate income tax they have to declare at the end of the year.

- General tax rate (20%): The same tax rate applies to most businesses.

Preferential tax rates based on revenue (Applicable from the 2025 tax year): The new law expands the scope of those eligible for lower tax rates based on the following criteria: total annual revenue:

- Level 15%: This applies to businesses with total annual revenue not exceeding 3 billion VND.

- Level 17%: This applies to businesses with total annual revenue ranging from over 3 billion VND to no more than 50 billion VND.

Conditions for determining “Total Revenue”: The total revenue used to determine this tax rate includes both revenue from financial activities and other income from the immediately preceding tax year (with specific regulations for newly established businesses).

- Special tax rates (25% – 50%): These apply to specific activities such as the search, exploration, and exploitation of oil, gas, and rare resources. For businesses trading in gold, silver, and precious stones, the standard tax rate 20% is usually applied, except in cases where there are other specific incentives (if any) based on industry or location. Corporate income tax declarations for these activities require a clear distinction between income and expenses.

Alongside changes in corporate income tax rates, businesses also need to pay special attention to updates related to deductible and non-deductible expenses. This directly affects taxable income and the amount of tax payable, so understanding it is crucial.

Update Deductible and Non-Deductible Expenses

The regulations regarding deductible expenses are central to determining taxable income.

Deductible expenses

Expenses that are deductible when determining taxable income must meet three basic conditions, which remain unchanged:

- These issues arise in practice in relation to the business operations of the enterprise.

- All invoices and supporting documents are in accordance with the law.

- Non-cash payment documents are required for transactions valued at 20 million VND or more (including VAT).

Non-deductible expenses under the Corporate Income Tax Law 2025

The new law has amended, supplemented, and emphasized approximately 37 expenses that are not deductible when calculating taxes. Businesses should pay particular attention to the following expense groups when declaring corporate income tax:

- Non-related expenses: Expenses that do not directly contribute to revenue generation or business operations.

- Excess expenses: Expenses exceeding the prescribed limits (e.g., welfare expenses, advertising or marketing expenses, interest on loans for GDLK).

- Salary expenses: Expenses for salaries and wages that are not specifically stated in the employment contract, collective bargaining agreement, or company's financial regulations, where the conditions and amounts of entitlement are not clearly specified.

Regulations regarding losses and loss carryforward

Businesses incurring losses are allowed to carry forward the entire and continuous amount of those losses from their business operations to taxable income in subsequent years.

- Loss carryforward period: No more than 5 years, starting from the year immediately following the year in which the loss was incurred.

- How to prepare a corporate income tax return for a loss: If a business incurs a loss in the tax year, it must still submit the tax return form 03/TNDN, recording the loss amount and using Appendix 03-2/TNDN (Loss Carryforward) to track the carried-forward loss.

After clearly understanding deductible and non-deductible expenses in corporate income tax, the next step for businesses is to grasp the entire process. Therefore, the following section will provide a detailed guide to the corporate income tax declaration and settlement process, helping you apply it correctly, minimize risks, and optimize your tax obligations effectively.

Details of the corporate income tax declaration and settlement process.

The corporate income tax filing process is a closed cycle, beginning with provisional payments during the year and ending with the annual tax settlement.

Quarterly provisional corporate income tax return

As mentioned, quarterly corporate income tax filing means that businesses determine the amount of tax payable themselves, rather than submitting a tax return.

- Regulations on provisional payment: Based on Decree 126/2020/ND-CP, enterprises shall determine the amount of provisional corporate income tax (if any) to be paid into the state budget.

- Penalties for underpayment: This is the biggest risk. Businesses must pay the full amount of corporate income tax due according to the annual tax return no later than the 30th of the first month of the fourth quarter. That is, if the total tax paid provisionally for the four quarters is less than the annual tax return, the business must pay late payment penalties on the shortfall from the day following the last day of the fourth quarter tax payment deadline.

The deadline for making quarterly advance payments is as follows:

- Quarters I, II, and III: No later than the 30th of the first month of the following quarter.

- Fourth Quarter: There is no specific deadline for submission, but the total for all four quarters must reach 80% of the annual settlement amount to avoid penalties.

After completing the quarterly provisional corporate income tax return and gaining a relatively clear picture of tax obligations for the year, businesses need to move on to the more important step of preparing the Annual Corporate Income Tax Final Settlement File. This is the crucial stage, determining the final amount of tax payable and the level of compliance of the business with the tax authorities.

Prepare Corporate Income Tax Return for the year

Corporate income tax settlement is mandatory and serves as the basis for tax authorities to verify a company's tax obligations.

Deadline for submitting the Corporate Income Tax Return (Tax Filing Period):

- No later than the last day of the third month following the end of the calendar year or fiscal year.

For example: For the corporate income tax period of 2025 (ending December 31, 2025), the deadline for payment is March 31, 2026.

Data preparation steps

To ensure the corporate income tax filing process is accurate and consistent, businesses need to complete the following data preparation steps:

- Step 1: Complete the Financial Statements: Prepare the financial statements (including the Balance Sheet, Income Statement, Cash Flow Statement, and Notes to the Financial Statements) according to Circular 200/2014/TT-BTC or Circular 133/2016/TT-BTC.

- Step 2: Review and Adjust Tax Expenses: Classify and exclude non-deductible expenses according to the Corporate Income Tax Law 2025 (Section 4.2). Make adjustments to increase or decrease Accounting Profit to determine taxable income.

- Step 3: Summarize Tax Incentives: Identify any tax-exempt income or income subject to preferential tax rates (if any).

After the business has completed the data preparation and document review, the next step is to prepare the Tax Return using the HTKK software, including Form 03/TNDN and related appendices. This is a crucial stage in transferring all standardized data into the form in accordance with the tax authority's regulations.

Prepare the Tax Return Form using the HTKK software (Form 03/TNDN and Appendix).

Instructions for filing corporate income tax returns on the HTKK software are the final and most important step. Businesses use the Tax Declaration Support Software (HTKK) of the General Department of Taxation to prepare their corporate income tax return.

The official declaration form 03/TNDN according to Circular 80/2021/TT-BTC

This form is the final result of the entire calculation process. Businesses need to fill it out accurately:

- Indicator A1: Total accounting profit before tax.

- Criterion B1: Adjustment of taxable income (from Appendices 03-1A, B, C).

- Criterion C1: Taxable income from business activities

- Indicator D1: Applicable corporate income tax rate (20% or preferential rate 15%, 17%).

Appendix to the Business Performance Report Form 03-1A/TNDN

This is a mandatory appendix for manufacturing, trading, and service businesses. This appendix helps to reconcile and adjust Accounting Income to Taxable Income according to tax law.

- Transfer the Revenue and Expense figures from the Income Statement to Part I (Determining Accounting Profit).

- Part II: Making adjustments (increases or decreases) to non-deductible expenses and tax-exempt income.

Appendix for Loss Carryforward Form 03-2/TNDN

If a business has losses carried forward, a detailed declaration is required:

- Column [06] records the number of losses carried forward from previous years (maximum 5 years).

- Column [08] records the amount of losses carried forward in this tax period to reduce taxable income.

Preferential Appendices (Forms 03-3A, 3B, 3C/TNDN)

Declare income from activities eligible for preferential tax rates (10%, 15%, 17%) or those exempt from or eligible for reduction of corporate income tax.

Appendix to Related Party Transactions

Businesses with related-party transactions during the year are required to submit the related-party transaction appendices along with Form 03/TNDN as per Decree 132/2020/ND-CP (Appendices I, II, III, IV), except in cases where they are exempt from declaring related-party transactions according to Article 19 of Decree 132/2020/ND-CP.

Note: Businesses with related-party transactions face transfer pricing risks; therefore, corporate income tax declarations related to related-party transactions need to be strictly controlled.

Tax-Exempt Income and Other Income

Businesses need to clearly distinguish between different types of income in order to declare corporate income tax correctly according to regulations.

Law 67/2025/QH15 continues to update and clarify tax-exempt income, including:

- Income from farming, livestock breeding, aquaculture, and seafood harvesting in particularly disadvantaged areas.

- Income from technical services directly related to agriculture.

- Income derived from performing tasks assigned by the state to certain organizations.

Regarding other income, this refers to income not related to the main business activities, but which is still subject to corporate income tax (except in cases where it is exempt).

For example: Income from capital transfers, real estate transfers (must be declared separately in Appendix 03-5/TNDN), interest on deposits, loans, and income from abroad.

Common mistakes when filing corporate income tax returns.

Common mistakes when filing corporate income tax returns can lead to unnecessary penalties.

During the corporate income tax filing process, businesses are prone to making mistakes due to missing documents, misunderstanding regulations, or incorrectly applying tax authority guidelines. To help businesses clearly identify and prevent these errors early on, the table below summarizes the most common types of errors with detailed descriptions.

| Error group | Content |

| Cost Errors | Insufficient invoices: Actual expenses incurred but lacking valid invoices/receipts.

Personal expenses: Expenses incurred for the personal use of the business owner or employee are considered deductible expenses. Depreciation: Incorrect depreciation calculation or depreciation of assets not used in production and business activities. |

| Errors in provisional payment | Making provisional payments under the amount of corporate income tax due according to the annual tax return is a common mistake, leading to late payment penalties. |

| Adjustments and supplementary declarations | Businesses are allowed to file supplementary tax returns under the Tax Administration Law 38/2019/QH14 when they discover errors.

If the amount of tax payable increases: Supplementary documents can be submitted at any time, but late payment penalties must be paid. If the tax liability is reduced or the loss is increased: Supplementary declarations may only be filed within 90 days of the annual tax return filing deadline or before a tax audit decision is made. |

Understanding common errors in corporate income tax declarations helps businesses proactively avoid risks, minimize disputes with tax authorities, and ensure a smoother tax settlement process. By effectively controlling each group of errors, businesses not only comply with the law but also optimize their tax obligations efficiently.

Handling violations and optimizing corporate income tax legally.

The detailed penalties for late submission of Corporate Income Tax returns are stipulated in Decree 125/2020/ND-CP, specifically as follows:

- Delay of 1 to 5 days (with mitigating circumstances): Warning.

- Delays of 1 to 60 days: Fines ranging from 2,000,000 VND to 5,000,000 VND.

- Late payment of 91 days or more: Fines ranging from VND 15,000,000 to VND 25,000,000 (applicable if all taxes have been paid before the inspection).

For acts of incorrect declaration resulting in underpayment of taxes (especially when declaring corporate income tax by improperly excluding or reducing income), penalties can range from 1 to 3 times the amount of tax evaded, or criminal prosecution in serious cases.

Regarding late payment penalties: Businesses must pay late payment penalties calculated on the amount of tax overdue at a rate of 0.03%/day on the overdue tax amount.

Conclusion and recommendations

2025 marks a significant period with the official entry into force of the Corporate Income Tax Law 2025. Filing corporate income tax returns is not only about compliance, but also an opportunity for businesses to review and restructure costs and take advantage of new tax rate incentives.

Businesses need:

- Stay proactive: Understand the changes to non-deductible expenses and new preferential tax rates (15%, 17%) to prepare for the 2025 tax year.

- Ensure compliance with related-party transactions: If there are related-party transactions, a complete plan and documentation in accordance with Decree 132/2020/ND-CP must be prepared before submitting the annual corporate income tax return.

- Managing provisional tax payments: Avoid the risk of late payment penalties due to not meeting the 80% threshold for annual tax settlement.

- To ensure that the corporate income tax filing process runs smoothly and accurately in accordance with the law, businesses should consider additional solutions. accounting services professional.

Businesses looking to minimize risks, optimize tax payments, and ensure accurate corporate income tax declarations should contact MAN – Master Accountant Network experts for prompt and precise support.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

MAN Editorial Board – Master Accountant Network