Construction accounting is always considered a "difficult problem" in the construction industry due to the inherent cost overruns, strict cost estimates, and high tax risks during final settlement. Even small errors in cost accounting, invoice timing, or acceptance record management can lead to disallowed expenses, tax arrears, and late payment penalties. Based on practical experience in implementing accounting for numerous construction projects and the latest legal regulations, this article will guide you through the entire process of construction accounting, from cost breakdown and aggregation to cost calculation, risk control, and tax settlement, ensuring safety and efficiency.

What is construction accounting?

Construction accounting is the process of tracking, aggregating costs, and calculating the cost of each specific construction project, project component, or contract package. The core objective is to accurately determine the profit/loss of each project based on actual figures compared to the initial estimate.

Unlike accounting in commercial or service businesses, construction accounting is organized by specific projects and items, focusing on tightly managing expenditures for materials, labor, machinery and equipment, as well as cash flow generated throughout the construction process. Due to the unique nature of construction activities, the construction accounting process is specifically designed, requiring a different approach to tracking, accounting, and controlling costs compared to conventional accounting models.

Job characteristics of a Construction Accountant

In construction companies, the job of a construction accountant has the following specific characteristics:

- Each construction project or item has its own winning bid estimate; therefore, accountants must break down and track costs independently for each project, avoiding combining figures.

- The cost items in a construction project are based on specific consumption norms, requiring accountants to calculate and control costs according to each component.

- Construction accountants compile costs to form bid prices based on the cost estimate provided by the engineering department, thereby determining the appropriate number and value of input invoices for accounting purposes.

- Construction costs vary depending on the construction site, as labor, material, and machinery rates differ between provinces and cities; accountants need to apply the correct pricing for each location.

- Most construction projects extend across multiple accounting periods, therefore accountants must closely monitor work-in-progress production costs for each project and each phase.

- The issuance of raw materials, tools, and equipment from inventory must adhere strictly to the approved budget norms to ensure reasonable costs during tax settlement.

- Upon completion of a project or item, the project accountant coordinates the preparation of acceptance and handover documents and issues invoices at the appropriate time according to regulations to record revenue.

The specific characteristics of project accounting, including cost estimates, cost standards, extended construction periods, and the need for strict document control, mean that project accounting goes beyond simply recording data. From this perspective, the role of project accountants is clearly demonstrated through each specific task, directly linked to construction progress, actual costs, and the tax obligations of the construction company.

What does the job of a construction accountant entail?

The role of a construction accountant is crucial in controlling cash flow and the financial performance of a construction company. By closely monitoring costs and revenues for each project, accountants help contractors optimize budgets, minimize the risk of exceeding estimates, and ensure that projects are implemented according to the financial commitments in the contract. So, in practice, what specific tasks does a construction accountant perform?

- Monitor, control, and supervise the financial situation of each construction project and item.

- Analyze, break down, and summarize the input material costs for each construction phase and specific item.

- Regularly update the project progress and compare it with the approved budget plan.

- Perform cost allocation and cost calculation for each item and each phase of the project.

- Manage labor schedules, prepare payrolls, and track labor costs at the construction site.

- Verify and review the validity and legality of accounting documents generated during the construction process.

- The organization maintains complete and legally compliant records and documents related to scientific projects.

- Evaluate and monitor the value of unfinished construction items to support cost calculation and financial reporting.

- Perform acceptance accounting, prepare and submit relevant reports as required by management.

- Coordinate with the investor in preparing project acceptance and final settlement documents.

- Combine costs and revenues to determine the profit or loss for each project.

- Collect and manage input invoices and prepare explanatory documents in case of inspections, audits, or tax settlements.

- Representing the business in dealings with government agencies within the scope of accounting services when necessary.

- Prepare monthly, quarterly, and annual financial and management reports to support the leadership's operational work.

As can be seen, the workload of a construction accounting job extends beyond simply recording data; it encompasses the entire lifecycle of a construction project, from preparation and construction to acceptance and final settlement. To effectively control costs, mitigate tax risks, and ensure that financial data accurately reflects reality, accountants need to perform this work according to a systematic, rigorous, and professionally standardized process. The following section will help you understand the detailed process of construction accounting and apply it effectively in your business.

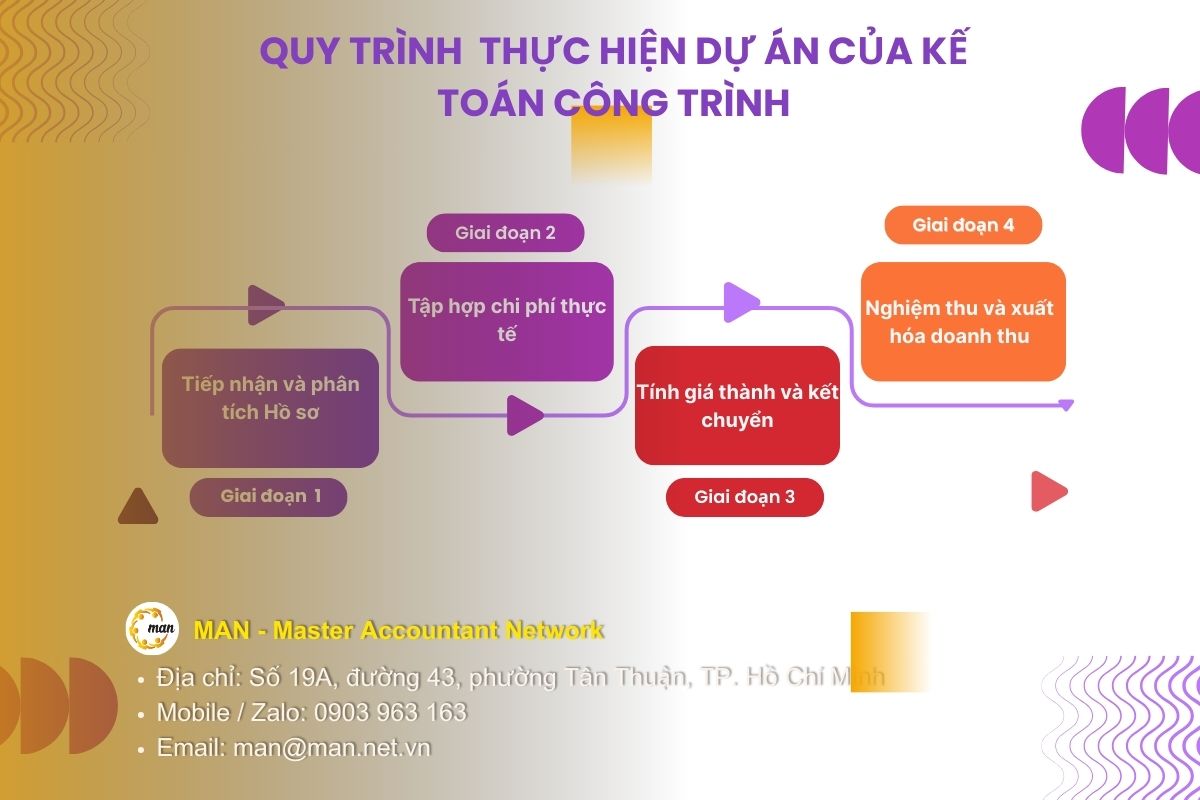

The project execution process of a Construction Accountant

To tightly control costs, minimize tax risks, and ensure that figures accurately reflect the actual construction process, construction accounting needs to adhere to a consistent workflow from project document receipt to acceptance and final settlement. This process not only helps accurately track each expenditure but also provides a basis for comparison with the budget and construction contract. Specifically, construction accounting is typically implemented through the following main stages.

Phase 1: Receiving and Analyzing Applications

Before construction begins, the accountant must have the Economic Contract and the Detailed Cost Estimate in hand.

Contract analysis:

- Determine the total value (including VAT and excluding VAT).

- Construction timelines and payment acceptance milestones.

- The percentage retained for construction warranty (usually 5%).

Construction accountants use the Cost Summary table to determine cost limits:

- Materials: How many tons of steel, cubic meters of sand, and bags of cement are needed?

- Labor: What is the total payroll budget for this project?

- Construction machinery: Costs for machine shifts, fuel, and outsourcing.

Phase 2: Gathering actual costs

This is the most time-consuming phase for construction accounting.

Direct material costs (Account 621)

Materials typically account for 60-70% of the total cost. There are two forms of purchasing:

- Direct purchase: Purchase from supplier and have them shipped directly to the construction site. Accounting entry: Debit Account 621, Debit Account 133 / Credit Account 331.

- Purchasing goods for inventory: Stored at the company and then gradually issued. Inventory receipt journal entry: Debit Account 152 / Credit Account 331; Inventory issue journal entry: Debit Account 621 / Credit Account 152 (details vary by project).

Direct Labor Costs (Account 622)

For salary expenses to be considered legitimate expenses, accountants need to prepare the following:

- Employment contract (seasonal or permanent).

- The time sheet at the construction site must be certified by the team leader/engineer.

- List of workers' national identity card numbers.

- Accounting entry: Debit account 622 (or 154) / Credit account 334.

Construction machinery costs (Account 623)

This includes fuel costs, machinery depreciation, or costs for leasing equipment from external sources.

- Depreciation: Debit Account 6234 / Credit Account 214.

- Fuel (Gasoline): Debit Account 6232 / Credit Accounts 111, 112, 331.

General production costs (Account 627)

These costs include: electricity and water at the camp, salaries for technical staff, and labor protection expenses…

- Accounting entry: Debit account 627 / Credit accounts 111, 112, 153, 334…

After all actual costs incurred at the construction site have been fully collected, correctly categorized into each item, and accurately accounted for for each project or item, the next step for accounting is to summarize and process the data to determine the actual cost. This is a crucial stage, helping businesses evaluate construction efficiency, control discrepancies compared to the budget, and serving as the basis for transferring costs and recording the cost of goods sold in accordance with accounting and tax regulations.

Phase 3: Cost Calculation and Transfer

At the end of the accounting period or upon completion of the project, follow these steps:

- When transferring expenses, the journal entry would be Debit Account 154 / Credit Accounts 621, 622, 623, 627.

- Calculate the cost:

|

Total cost = Beginning work-in-process costs + Costs incurred during the period – Ending work-in-process costs. |

- At the end of the year, the cost of goods sold is transferred as follows: Debit Account 632 / Credit Account 154.

After all costs have been collected, allocated, and transferred to determine the actual cost of the project or item, this is only the final step in terms of internal costing. For this value to be officially recorded in the accounting books and generate tax obligations, the business needs to move to the next stage: the acceptance of completed work and the issuance of invoices to record revenue at the prescribed time.

Phase 4: Acceptance and issuance of revenue invoices

The time of invoicing for construction is the time of acceptance and handover of the item or the entire project (regardless of whether payment has been received or not). At that time, revenue is recorded as Debit Account 131 / Credit Account 511, Credit Account 3331.

However, completing the correct construction accounting process from cost collection and cost calculation to acceptance and invoice issuance is not the final stage. In reality, even a small error in VAT, material specifications, or acceptance documents can cause all recorded costs to be disallowed during final settlement. Therefore, in addition to accounting practices, construction companies need to pay special attention to tax control and risk management throughout the construction process.

Tax control and risks in construction.

In the construction industry, tax and legal risks are always present if businesses don't maintain strict control from the outset. Understanding VAT regulations, managing costs according to established standards, and preparing complete settlement documents not only helps businesses avoid tax arrears and disallowed expenses but also protects accounting data during tax audits and inspections. Below are key areas that construction accountants need to pay special attention to in order to proactively control taxes and mitigate risks during construction.

Temporary VAT (Outside the province)

According to Circular 80/2021/TT-BTC, if the project is located in a province different from where the head office is located, the enterprise must pay temporary VAT (usually 1% on revenue before tax). This tax amount will be deducted from the tax payable at the head office.

Managing "phantom" and over-quantity materials.

Tax authorities typically compare the actual inventory withdrawals with the projected figures.

- If there is an excess of the cost: The expense will be disallowed.

- If invoices are underpaid: This may raise suspicions of invoice manipulation or substandard construction quality.

- Solution: Regularly reconcile monthly figures between the accounting department and engineers to ensure timely record adjustments.

What documents are needed for tax settlement?

To protect your data from the inspection team, you need to organize it into separate project files:

- Contracts, contract addendums.

- Approved design documents and cost estimates.

- Construction log.

- Minutes of acceptance of work volume, minutes confirming the completion of work volume.

- AB settlement documents.

Conclude

Construction accounting goes beyond simply recording expenses or preparing reports; it's a comprehensive management process encompassing cost estimation, construction, acceptance testing, and tax settlement. In the context of increasingly stringent tax and invoicing policies, understanding and implementing these processes correctly from the outset will help businesses effectively control costs, mitigate legal risks, and safeguard profits for each project. If your business is struggling with documentation, cost control, or needs to review data before final settlement, proactively addressing these issues is essential. exchange With MAN – Master Accountant Network, you'll find a safe and time-saving solution. Don't let small mistakes in construction project accounting become major risks for your business later on.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about Construction Accounting

How can you monitor an unfinished project that has dragged on for three years?

You record all expenses in account 154. Each year, you must still conduct an inventory of work-in-progress to determine the value of inventory on the balance sheet. Do not transfer to account 632 unless the project has been partially or fully accepted.

What about outsourced labor costs that don't have invoices?

Businesses can enter into subcontracting agreements with individuals or groups of workers. If the total income exceeds 2 million VND per payment or per month, personal income tax (PIT) must be deducted before payment.

Is it permissible to issue an invoice for a value lower than the contract value?

Yes, if the actual volume of work completed is less than initially planned. This is evidenced by the actual work volume acceptance report.

MAN Editorial Board – Master Accountant Network