The latest Form 01/GTGT (2026) is the mandatory value-added tax declaration form for businesses applying the deduction method, in the context of the 2024 VAT Law and Decree 181/2025/ND-CP officially coming into effect. Understanding the form correctly, its legal basis, tax calculation methods, and payment deadlines is crucial not only for accurate tax declarations but also for minimizing the risk of tax arrears and penalties. This article provides a comprehensive guide to filling out the latest Form 01/GTGT (2026), the payment deadlines stipulated by the Government, and important notes that businesses should pay special attention to in 2026.

What is the latest 2026 form 01/GTGT?

As of the current date in 2026, the latest Form 01/GTGT (Value Added Tax Declaration Form 2026) remains the value-added tax declaration form issued with Circular No. 80/2021/TT-BTC of the Ministry of Finance. Although the Government has issued new decrees guiding the 2024 VAT Law, the declaration forms in Circular 80/2021/TT-BTC are retained to ensure stability in administrative management.

| Download the latest Form 01/GTGT |

Applicable objects

This form is specifically for taxpayers who calculate taxes using the deduction method and are engaged in production and business activities. This is the most common method for businesses and organizations with stable revenue and a complete accounting system.

Basic structure of the declaration form

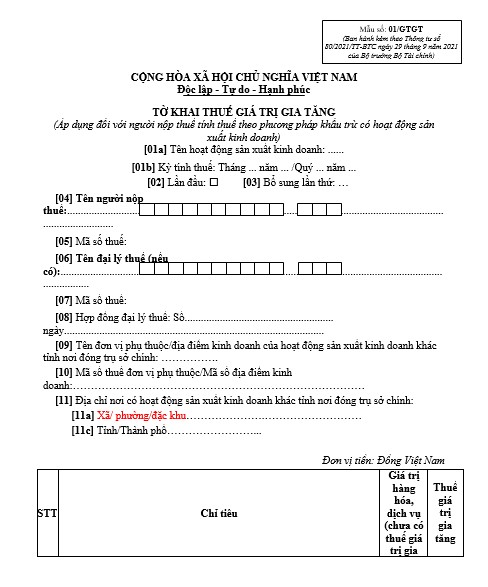

Form 01/GTGT includes the following main sections:

- General information: Tax identification number, taxpayer's name, tax period.

- Part A: Purchased Goods and Services: Reflects the total value and tax amount of goods purchased during the period.

- Part B: Goods and services sold: Reflects revenue and output tax at each tax rate.

- Part C: Determining Tax Liabilities: Calculate the amount of tax that can be carried forward to the next period as a deduction or the amount of tax payable.

Key legal basis of the Government applicable for the year 2026

To accurately fill out the latest 2026 Form 01/GTGT, taxpayers need to pay special attention to the following three legal pillars issued by the Government and the National Assembly:

Law on Value Added Tax No. 44/2024/QH15

This is the highest legal document on VAT, which will come into effect and directly affect the tax year 2026. This law includes important amendments regarding:

- List of items not subject to VAT.

- Stricter regulations are being implemented regarding non-cash payment documents required for input tax deductions.

- Preferential tax rates are applied to specific product categories.

Government Decree 181/2025/ND-CP

The government has issued Decree 181/2025/ND-CP to provide detailed regulations for the implementation of several articles of the 2024 Value Added Tax Law. This is the most important technical guidance document, replacing previous decrees (such as Decree 209/2013/ND-CP). Details regarding the tax base and the timing of VAT determination are all specified herein.

Circular 80/2021/TT-BTC

Although issued in 2021, the regulations on tax declaration forms, tax refund procedures, and especially the system of forms in this Circular still serve as the standard for businesses to present data to the Tax authorities.

Instructions on how to calculate VAT payable according to the latest regulations.

Based on Article 20 of Government Decree 181/2025/ND-CP, the tax calculation formula for businesses using the latest Form 01/GTGT (2026) is determined as follows:

|

VAT payable = Output VAT – Input VAT eligible for deduction |

Determine the output VAT amount.

Output tax is the total tax on goods and services sold as recorded on the value-added tax invoice. According to the Government's guidance in Decree 181/2025/ND-CP, the specific formula is:

|

VAT on invoice = Taxable price x Tax rate (%) |

In cases where the invoice price includes tax (the payment price), the accountant must convert it back to find the taxable price.

|

Price excluding tax = Payment price / (1 + Tax rate) |

Determine the amount of deductible input VAT.

This is where errors frequently occur, leading to tax arrears. To be eligible for deduction, input tax must fully meet the conditions in Article 4 of the Value Added Tax Law 2024:

- There must be a valid value-added tax invoice or proof of payment of import VAT.

- There must be non-cash payment documents for purchased goods and services (except for low-value cases as stipulated by the Government).

- Specifically for outsourced services, tax payment documents must be provided as stipulated in Point a, Clause 2, Article 3 of Decree 181/2025/ND-CP.

Deadline for submitting VAT tax returns for Quarter IV/2025

Compliance with tax filing deadlines is a mandatory requirement under the Government's Tax Administration Law.

Deadline for filing tax returns for Q4/2025

Normally, the deadline for filing quarterly returns is the last day of the first month of the following quarter. For Q4/2025, the theoretical deadline is January 31, 2026. However:

- January 31, 2026 falls on a Saturday (a public holiday).

- Based on Article 86 of Circular 80/2021/TT-BTC and the Civil Code, if the deadline coincides with a holiday, the deadline will be extended to the next working day.

The deadline for submitting the latest Form 01/GTGT 2026 for the fourth quarter of 2025 is February 2nd, 2026 (Monday).

Detailed instructions for filling out the information on the latest 2026 Form 01/GTGT.

To properly complete the latest Form 01/GTGT 2026, accountants need to pay attention to the following key indicators:

Input tax indicators (Indicators [21] to [25])

To accurately determine the amount of input VAT deductible in the period, accountants need to fully and correctly declare the indicators from [21] to [25] on the latest Form 01/GTGT 2026, in which each indicator specifically reflects the purchase value and the amount of tax that meets the conditions for deduction as prescribed by the Government.

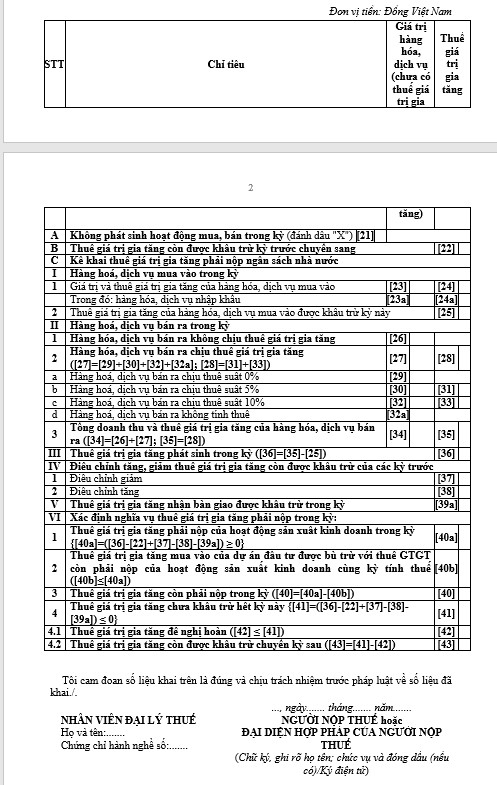

- Indicator [21] – No buying or selling activities during the period: If during the declaration period the business establishment does not have any buying or selling activities of goods or services, it must still prepare a declaration and send it to the tax authority. On the declaration form, the business establishment selects “X” in box [21].

- Indicator [22] – VAT tax still deductible from the previous period carried over: Point to note, the tax payable or overpaid in the previous period should not be recorded in this indicator box. If in the previous period, the business underpaid the tax, it must complete the remaining tax amount in the State Budget. If the input tax deductible is greater than the output tax, the greater deduction will be calculated for the next period.

- Indicator [23] – Value of purchased goods and services: This indicator reflects the total value of goods and services purchased during the tax period, determined at prices excluding VAT, including both domestic purchases and import transactions. According to Circular 80/2021/TT-BTC, the current form has added indicator [23a] to separate and clearly show the value of imported goods and services when making declarations.

- Expenditure [23a] – Value of imported goods and services: Reflects the total value of imported goods and services incurred during the period, recorded at prices excluding VAT. The declared figures are determined on the basis of legal import documents such as customs declarations that have been cleared, import contracts, invoices issued by foreign partners and related documents as prescribed.

- Indicator [24] – Total VAT of purchased goods and services: Reflects the total VAT generated from purchased goods and services during the period, including both the deductible and non-deductible portions as prescribed. At the same time, the accountant must also declare the VAT actually paid at the import stage during the period in this indicator.

- Expenditure [24a] – VAT on imported goods and services: Note When filling in this section, if a business purchases goods or services originating from abroad but does not directly carry out import procedures and does not use an import consignment arrangement, this transaction is considered a domestic purchase. Accordingly, the accountant does not declare the value arising from this transaction in this section on the VAT tax return.

- Expenditure [25] – VAT of goods and services purchased that are deductible this period: Total value-added tax generated from goods and services purchased during the period that fully meet the conditions for deduction according to the law. The accountant only declares the VAT that is eligible for deduction; the VAT that is not eligible for deduction is not recorded in this item.

Group of indicators on revenue and output tax (Indicators [26] – [35])

This group reflects all taxable revenue generated during the period and serves as the direct basis for determining the output VAT payable. When declaring this group of indicators, accountants need to accurately classify revenue according to each tax rate and taxable entity as stipulated by the Government, specifically as follows:

- Indicator [26] – Goods and services sold not subject to VAT: The data to be filled in this box is the total value of goods and services sold during the period that are not subject to VAT of the establishment

- Indicator [27] – Goods and services sold subject to VAT: Determined by the formula: [27] = [29] + [30] + [32] + [32a]

- Expenditure [28] – VAT on goods and services sold: The data to be filled in this box is the total output VAT corresponding to the total value of goods and services sold subject to VAT as filled in item [27]. Calculation formula [28] = [31] + [33]. Special attention is needed.Each item and service has a different VAT rate, so it must be declared according to the prescribed rate.

- Indicator [29] – Goods and services sold subject to VAT rate 0%: The data to be filled in the box is the value of goods and services sold during the period subject to VAT rate 0%.

- Indicator [30] – Goods and services sold subject to VAT rate 5%: The data to be filled in the cell is the value of goods and services sold during the period subject to VAT rate 5%

- Indicator [31]: Fill in the corresponding value as in indicator [30]

- Indicator [32] – Goods and services sold subject to VAT rate 10%: The data to be filled in the box is the value of goods and services sold during the period subject to VAT rate 10%

- Criterion [32a] – Goods and services sold that are not subject to tax: Record the value of goods and services sold (not subject to VAT) that do not need to be declared, calculated, or paid tax.

- Indicator [33] – VAT of goods and services sold subject to tax rate 10%: Fill in the corresponding data as in indicator [32].

Then the total revenue and VAT of goods and services sold [34] = [26] + [27]; [35] = [28].

VAT incurred during the period is determined [36] = [35] – [25], if:

- The [36] indicator is positive if there is VAT payable.

- Negative [36] indicator is the amount of input VAT in the period that has not been fully deducted. Businesses can transfer the deduction to the next period or receive a refund if it is the correct subject and meets the conditions.

Adjusting the increase or decrease in deductible VAT from previous periods.

The indicators in this section are shown as follows:

- Item [37] – Adjustment to reduce deductible VAT of previous periods: In supplementary declarations of previous periods, if a difference arises that reduces the amount of deductible VAT, this reduced difference must be recorded in item [37] on the declaration form of the current declaration period.

- Indicator [38] – Adjustment of VAT to increase the deductible VAT of previous periods: Supplementary declaration of previous periods, if it results in an increase in the amount of VAT that is still deductible, must be declared in indicator [38] of the current period.

VAT received upon handover is deductible in the period.

Indicator [39a] on the VAT tax return according to Circular 80 is used to reflect the amount of VAT that is still deductible but not yet refunded, carried forward for taxpayers to continue deducting in subsequent periods. This tax may arise from an investment project that has been separately declared but does not meet the refund conditions and is carried forward when the project officially comes into operation, or from the production and business activities of a subsidiary unit when this unit ceases operation.

The declaration of indicator [39a] is intended to serve the monitoring and comparison of VAT amounts transferred between relevant units, thereby helping the tax authority to closely control the accuracy of recording and deducting input VAT, limiting the risk of over-declaring the deductible tax amount of enterprises.

Determine the VAT tax liability payable for the period.

Indicators [40a] to [43] on Form 01/GTGT play a comprehensive role in directly determining the amount of VAT payable, the amount of tax refunded or deducted carried forward to the next period of the enterprise. When declaring this group of indicators, accountants need to clearly understand the meaning of each indicator, the conditions of application, and the calculation relationship between the cells on the declaration form to avoid confusion, especially in cases of offsetting investment projects or requesting tax refunds. The table below will provide detailed instructions on how to determine and use each indicator in accordance with current regulations.

| Target | Content | How to identify and note |

| [40a] – Value Added Tax payable on business activities during the period | This reflects the amount of VAT payable arising from production and business activities during the tax period. This indicator is automatically determined by the tax declaration system based on related indicators. | Formula: [40a] = ([36] – [22] + [37] – [38] – [39a])

If the result is negative, enter 0. |

| [40b] – Input VAT of investment projects is offset | This applies to businesses that declare taxes using the deduction method, have investment projects located in the same area as their head office, and file separate tax returns for the projects during the investment phase. | The value [40b] is taken from indicators [28a], [28b] of declaration form 02/GTGT and must not exceed [40a]. Mandatory condition: [40b] ≤ [40a]. |

| [40] – VAT still payable in the period | This shows the final VAT amount that the business must pay to the state budget in the period after offsetting eligible amounts. | Determined by formula: [40] = [40a] – [40b]

Businesses are not allowed to offset any remaining deductible tax from the next period. |

| [41] – VAT not fully deducted this period | This reflects the amount of input VAT exceeding output VAT during the period, which has not been fully deducted and is eligible for further processing. | Calculation formula: ([36] – [22] + [37] – [38] – [39a]) ≤ 0. If the result is negative, the software displays a positive number. When [41] is present, [40] does not occur. |

| [42] – VAT refund requested | Record the amount of uncredited VAT that the business proactively requests a refund for during the period, if it meets the conditions stipulated by tax law. | Value [42] ≤ [41]. If this indicator is declared, the enterprise is required to submit a dossier and a letter requesting a tax refund. The amount requested for refund cannot be carried over to the next period. |

| [43] – VAT that is still deductible carried forward to the next period | This shows the remaining VAT amount that has not been fully deducted after subtracting the amount already requested for refund, which is carried over to the next period for continued deduction. | Calculation formula: [43] = [41] – [42]. This data will be transferred to indicator [22] of the next tax declaration period. |

The indicators from [40a] to [43] are closely related and are automatically calculated by the software based on declared accounting data. However, accountants still need to carefully check the application conditions of each indicator, especially in cases of offsetting investment projects or requesting tax refunds, to ensure that the data accurately reflects reality and complies with current regulations. Understanding the true nature of each indicator will help businesses minimize errors, avoid the risk of being subject to tax collection, and be proactive in tax settlement.

Conclude

Updating and correctly implementing the latest Form 01/GTGT (2026) is a critical requirement for every business in 2026. With the introduction of the 2024 VAT Law and Decree 181/2025/ND-CP, the Government has created a more transparent legal framework but also demands higher compliance from taxpayers. Hopefully, this article has provided you with a comprehensive overview and the most practical guidance to confidently carry out the upcoming tax settlement period.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

MAN Editorial Board – Master Accountant Network