According to Resolution 198/2025/QH15, from January 1, 2026, household businesses and individual businesses will no longer be subject to the lump-sum tax method. Instead, all entities subject to this regulation must fulfill their tax obligations using the declaration method.

This regulation marks a significant change in tax policy, aiming to enhance transparency, accurately reflect actual revenue, and improve management efficiency for the household economic sector.

Subjects and timing of mandatory switch to the declaration method.

The conversion process does not apply uniformly to all business households but is determined based on the scale of operation, especially revenue and the number of employees. Therefore, business households need to clearly understand the application conditions and conversion timelines to avoid incorrect declarations or administrative penalties for tax violations.

This group of household businesses is subject to mandatory declaration.

Large-scale business households and individual businesses, or those with annual revenue ranging from 500 million VND to 3 billion VND (depending on the production and business sector), will be prioritized for transitioning from the lump-sum method to the declaration method.

The implementation of tax declaration aims to ensure that the tax payable accurately reflects actual expenses, limiting the outdated practice of fixed-rate tax assessments.

The official start date for filing taxes.

One of the issues of concern to many businesses is whether they are required to make retroactive declarations for the period at the end of 2025. According to Resolution 198/2025/QH15, this matter is clearly defined as follows:

- In 2025: Household businesses will continue to pay taxes using the lump-sum method; there will be no changes.

From 2026, household businesses will officially switch to the declaration method, specifically:

- If filing monthly: The first filing period is January 2026.

- If filing quarterly: The first filing period is Quarter I/2026

RemarkableTherefore, there is no obligation to file a retroactive tax return for the fourth quarter of 2025, as this period still falls within the timeframe for applying the lump-sum tax.

The process of converting from a household under the lump-sum tax system to a household under the declaration system.

From January 1st, 2026, business households subject to conversion must complete the necessary procedures as prescribed to finalize the application of the declaration method, ensuring full compliance with tax obligations in the new period.

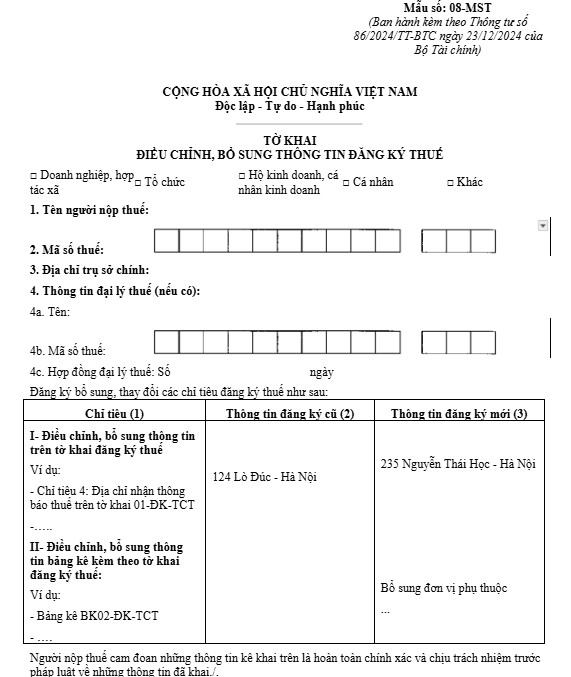

Tax calculation method change application

Household businesses must notify the tax authorities of the change in tax calculation method by completing Form 08-MST as prescribed in Circular 86/2024/TT-BTC and submitting it to the tax authority directly managing them to register for the switch from the lump-sum tax method to the declaration method.

Inventory at the time of transition

Before officially implementing the inventory declaration method, business households need to review and inventory all goods they have at the beginning of the period. The inventory must include both goods with legal documentation and goods without invoices.

The inventory results are recorded in a confirmation report, which serves as the basis for determining the opening inventory balance and is recorded in the accounting system from January 1, 2026.

Register and start using electronic invoices.

Depending on their business model, household businesses choose the appropriate type of electronic invoice:

- Direct retail sales to consumers: Register to use electronic invoices generated from cash registers, meeting the connection and data transmission requirements as stipulated by the tax authorities.

- For service provision or wholesale activities: Register to use electronic invoices with tax authority codes, through licensed electronic invoice solution providers.

Organize the accounting system and records in accordance with regulations.

When switching to the declaration-based method, business households are responsible for opening and maintaining complete accounting books as guided by Circular 88/2021/TT-BTC. Specifically, at a minimum, the following books must be maintained:

- General journal: Reflects all economic transactions as they occur in chronological order.

- Revenue Ledger: Separately tracks revenue from the sale of goods and provision of services.

- Inventory ledger: Records the import, export, and inventory status of materials, tools, equipment, and goods.

- Production and business cost tracking ledger: Used to determine operating results.

- Tax obligation tracking register: Manages taxes payable and paid to the state budget.

- Payroll and insurance record book: Detailed record of obligations to employees.

Cash and bank deposit ledger: Reflects the situation of income and expenses and fluctuations in cash flow.

Schedule for filing and paying taxes using the new method.

Meeting tax filing and payment deadlines is crucial for businesses to minimize the risk of penalties for late payments, while ensuring smooth and compliant fulfillment of tax obligations.

| Criteria | Monthly declaration | Quarterly declaration |

| Applicable objects | Household businesses with revenue exceeding 50 billion VND in the preceding year. | Household businesses with revenue of 50 billion VND or less in the preceding year. |

| Tax return | Form 01/CNKD with Appendix 01-2/BK-HĐKD | Form 01/CNKD with Appendix 01-2/BK-HĐKD |

| Deadline for submitting the declaration | No later than the 20th of the following month | No later than the 30th of the first month of the following quarter |

| Tax payment deadline | Same deadline for submitting the declaration | Same deadline for submitting the declaration |

Determining the correct tax filing method—monthly or quarterly—is crucial for business households transitioning to this method. The primary basis for this choice is the revenue of the preceding year, which in turn determines the appropriate deadline for filing and paying taxes.

Complying with regulations from the outset not only helps businesses avoid penalties for late payments or incorrect declarations, but also lays the foundation for transparent, stable, and long-term financial management in the context of increasingly stringent tax policies.

Instructions for converting online lump-sum tax to declaration tax for household businesses.

Business owners can register for the conversion through the Tax Department's Public Service Portal with the following detailed steps:

Step 1 – Log in to the electronic system

Access the tax authority's electronic portal at this address. dichvucong.gdt.gov.vnNext, log in using your personal electronic tax account or the business tax code issued by the tax authority to proceed with the relevant procedures.

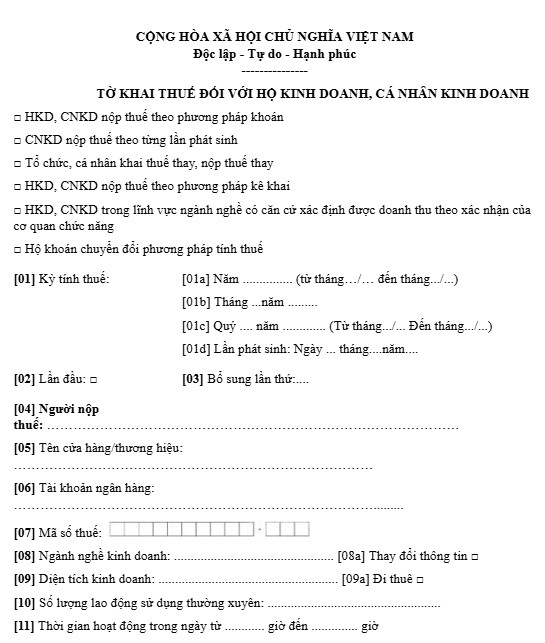

Step 2 – Choose the appropriate declaration form.

On the system's management screen, taxpayers access the Administrative Procedures function, then select the Declaration form. Next, they enter their tax identification number so the system can automatically look up and display the relevant procedures.

In the list of results, taxpayers can search by procedure code 2.002259 or directly select Form 01/CNKD – Tax declaration form applicable to individual businesses, issued together with Circular 40/2021/TT-BTC.

| Download Form 01/CKND |

Step 3 – Confirm business location and select filing period

After selecting the appropriate tax declaration form, the business household needs to accurately determine the location where its production and business activities take place, based on the information registered with the tax authorities.

Next, taxpayers choose either monthly or quarterly tax filing periods, based on their revenue from the preceding year. Choosing the correct filing method is crucial to ensuring the proper acceptance of the tax return and avoiding future adjustments.

Step 4 – Declare the method conversion and complete the electronic signing.

In the declaration section, business households must mark their confirmation of switching from the lump-sum method to the declaration method in accordance with regulations. Simultaneously, they must declare the estimated revenue for the first declaration period, corresponding to Quarter 1 of 2026 or January 2026, depending on the chosen declaration method.

After reviewing all the information, taxpayers digitally sign the tax return using a USB Token or remote electronic signature, then submit the documents through the system to complete the procedure.

Key points to note regarding documentation and financial management.

According to current regulations, after switching to the declaration method, business households need to ensure compliance with the following requirements:

Requirements for invoices and supporting documents.

Since the implementation of the declaration method, all purchases of goods and services for business operations must be supported by valid invoices and documents. This is an important basis for tax authorities to accept expenses during audits and inspections.

Manage payment accounts

Household businesses are required to open a separate bank account for their business operations, distinct from personal expenses. This account is to be used for transactions of 20 million VND or more, in accordance with cashless payment requirements.

Social insurance obligations

When switching to the declaration-based system, household businesses incur the responsibility of registering and paying social insurance for their employees and for the household owner themselves (if eligible), in accordance with the current regulations of the Social Insurance Law.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.