Starting January 1, 2026, the tax mechanism applied to household businesses will undergo a fundamental change as the lump-sum tax method will no longer be used. This is considered a major shift in tax management and also raises many concerns for small businesses, those with low revenue, or those operating in specialized fields such as solar power production and small-scale services.

In this context, understanding the new tax declaration procedures, accounting obligations, and regulations on the use of electronic invoices is crucial for businesses to comply with the law and minimize unnecessary expenses.

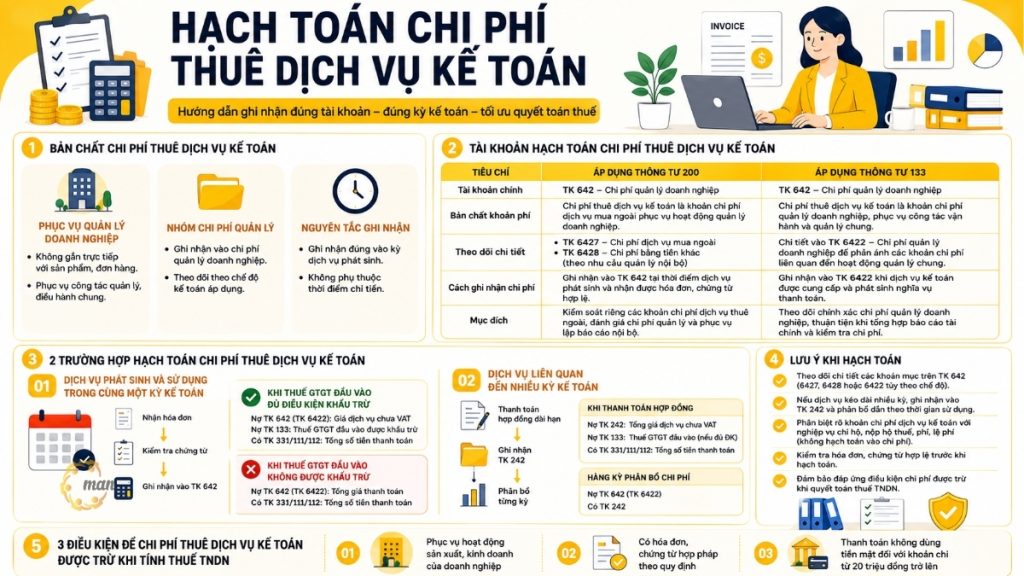

Legal basis for abolishing lump-sum tax from 2026.

According to Resolution No. 68-NQ/TW dated May 4, 2025, of the Politburo on the development of the private economy, the State has clearly defined the policy of ending the lump-sum tax system for business households no later than 2026. This policy aims to enhance transparency, promote digital transformation in tax management, and create conditions for business households to gradually transition to the enterprise model.

To implement the above policy, Decision No. 3389/QD-BTC dated October 6, 2025, of the Ministry of Finance approved the plan to innovate tax management methods, according to which business households must implement the self-declaration and self-payment mechanism from January 1, 2026. This means that the term "lump-sum tax" will no longer appear in the tax management system from this point onwards.

Comparing tax administration methods before and after the abolition of lump-sum tax.

To help businesses easily understand the changes in the tax management mechanism when the lump-sum tax is officially abolished from 2026, the table below summarizes and compares the important criteria between the previous method and the new declaration method. Through this, businesses can clearly identify the obligations arising, especially those related to tax declaration, accounting procedures, and the use of electronic invoices.

| Comparison criteria | Before 2026 | From January 1, 2026 |

| Tax calculation method | Applying a flat-rate tax to many small businesses. | 100% declares taxes based on actual revenue. |

| How to determine revenue | Revenue is determined by the tax authorities based on a fixed rate. | Revenue is based on actual invoices and supporting documents. |

| Declaration obligations | No regular declarations are required; payments are mainly based on a fixed rate. | Self-declaration and self-payment of taxes periodically. |

| Accounting regime | Not required or only very simple record-keeping. | The accounting system as stipulated in Circular 88 is mandatory. |

| Invoice format | You can use paper invoices or request individual invoices for each transaction. | The use of electronic invoices is mandatory when selling goods or providing services. |

| Level of management | Management based on estimates offers high stability but lacks transparency. | Transparent, digitized management that closely aligns with real-world operations. |

As the comparison table above shows, the abolition of lump-sum tax from 2026 is not only a change in tax calculation but also entails a comprehensive shift in the management method for household businesses. From being dependent on lump-sum amounts determined by the tax authorities, household businesses will have to be more proactive in record-keeping, revenue declaration, and the use of electronic invoices. Early preparation in terms of awareness, accounting procedures, and invoicing solutions will help household businesses adapt smoothly to the new mechanism, reduce risks, and avoid unnecessary costs during implementation.

Who is required to use electronic invoices and point-of-sale (POS) systems?

Based on the Law on Tax Administration No. 38/2019/QH14 and Decree No. 70/2025/ND-CP dated March 20, 2025, the obligation to use electronic invoices is classified as follows:

Household businesses file tax returns.

These are households with revenue and labor force meeting the criteria of a micro-enterprise or larger. This group must implement accounting procedures and use electronic invoices with tax authority codes for all sales and service transactions.

Businesses are required to use cash registers.

According to Clause 1, Article 11 of Decree 70/2025/ND-CP, only households with annual revenue of VND 1 billion or more, or those operating in the retail sector directly selling to consumers (food and beverage, restaurants, hotels, supermarkets, retail, etc.), are required to use electronic invoices generated from cash registers.

Guidelines for handling invoices for household businesses with revenue under 160 million VND.

For business households with total revenue in 2025 under VND 160 million, according to current regulations, there is no obligation to pay VAT in 2026. However, in practice, difficulties arise during the transition period, especially with revenue at the end of 2025 but invoices issued at the beginning of 2026 (for example, electricity bills for December 2025 finalized in January 2026).

Some common difficulties include:

- The tax authorities no longer issue individual invoices for each transaction to households that have switched to the declaration-based system.

- Despite low revenue, household businesses still need to equip themselves with electronic invoicing software to process outstanding invoices.

- The cost of purchasing the software (approximately 1 million VND) becomes a significant burden compared to the small revenue scale (for example, only 10-15 million VND/month).

Important notes during the transition to filing tax returns.

While detailed guidelines on handling individual invoices for household businesses are still being finalized, household businesses should proactively implement the following solutions:

- Contact the relevant tax office directly for the latest guidelines. Some localities may implement temporary solutions during the transition period.

- Prioritize choosing flexible electronic invoicing software that allows purchasing based on the number of invoices (50-100) instead of an annual package, in order to save costs if the need is not high.

- Implementing simplified accounting practices in accordance with Circular 88/2021/TT-BTC ensures clear and transparent data from the outset. This helps business households easily demonstrate lower actual revenue and avoid risks during tax audits.

- Closely monitor new guidelines related to the Tax Administration Law, especially regarding the mechanism for handling invoices arising unexpectedly for taxpayers – a topic that currently lacks detailed regulations.

Contact information MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Source: Vietnamese Law